Whatsapp

Whatsapp

Personal Guarantors Liable for Corporate Debt: Comprehending Supreme Court’s verdict.

Introduction

The provisions of the Insolvency and Bankruptcy Code, 2016 (IBC) regulating the obligation of personal guarantors to corporate debtors were affirmed in a recent decision by the Hon’ble Supreme Court in Lalit Kumar Jain v. Union of India. With the judgement in place, creditors can now file insolvency proceedings against people such as promoters, managing directors, and chairpersons who act as personal guarantors on loans made to corporate debtors or goods and services provided to them.

A personal guarantor is a person or an organization who agrees to pay another person’s debt if the latter fails to do so. This concept of ‘guarantee’ is derived from Section 126 of the Indian Contracts Act, 1872.[1] When banks want collateral that equals the risk they are taking by lending to a company that may not be performing well, a promoter or promoter entity is most likely to provide a personal guarantee. It differs from the collateral that businesses provide to banks in order to obtain loans, because Indian corporate law stipulates that individuals, such as promoters, are distinct from businesses, and that the two are distinct entities.

Brief Legal History

The Ministry of Corporate Affairs published a Notification on November 15, 2019, bringing personal guarantors into the scope of insolvency proceedings under the IBC. The goal was to hold the promoters of the defaulting enterprises accountable for providing personal guarantees for the loans taken out by their enterprises. The lenders filed bankruptcy claims against India’s leading business tycoons, including Anil Ambani, Kapil Wadhawan, and Sanjay Singal, in accordance with the requirements. Many promoters opposed the new laws in several high courts, alleging that the promoters alone should not be held accountable for loan repayment failure.

In October 2021, the Supreme Court reassigned to itself a slew of writ petitions contesting the IBC’s personal insolvency rules that had been pending in several high courts. When the government issued the notification on personal insolvency in December 2019, the provisions were challenged in court by as many as 19 promoters, who claimed that the company was always run by a management board and that the promoters alone should not be held liable for debt repayment default. As many as 75 promoters and guarantors had challenged the personal insolvency provisions by the time the Supreme Court moved all the cases to itself in December 2020.

Outlook of the petitioners

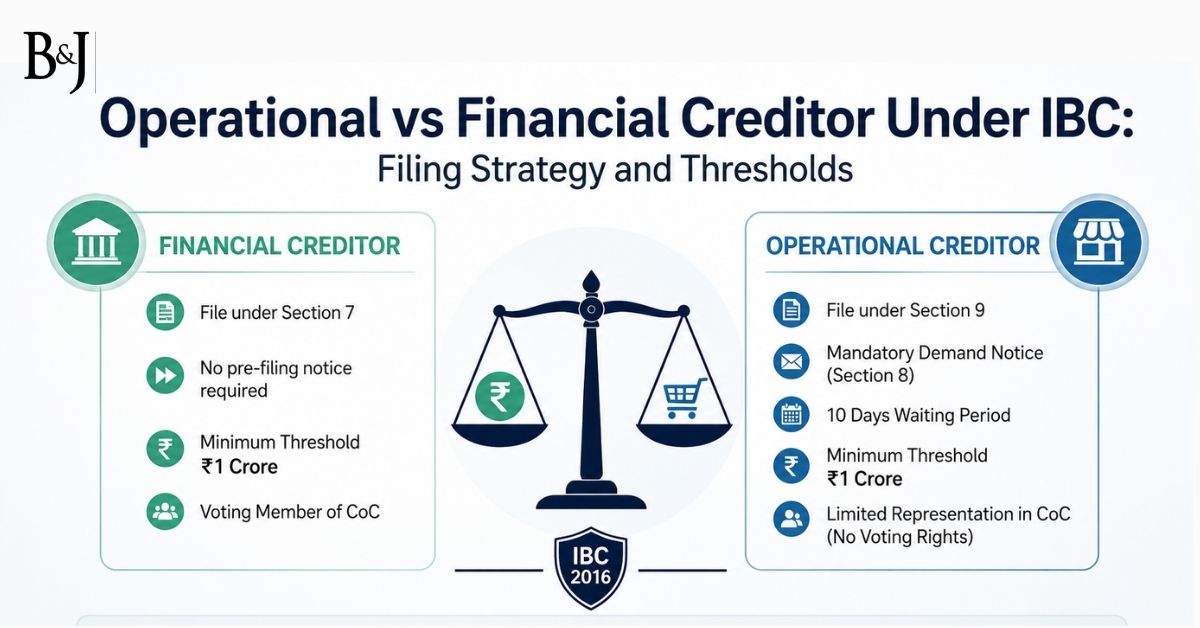

Firstly, the petitioners believed that the Central Government had overstepped its authority by issuing the Notification, which changed Part III of the IBC in an unjustifiable manner. . Because the legislature made the law in its entirety, leaving nothing for the executive to legislate on, it was referred to as “conditional” rather than “delegated.”[2] Further, the petitioners argued that the rules of the Notification, establish a single procedure for a personal guarantor’s insolvency resolution, regardless of whether the creditor is a financial creditor or an operational creditor. In Swiss Ribbons (P.) Ltd. v. Union of India,[3] the court determined that the nature of loan arrangements executed by a corporate debtor with financial creditors differed significantly from contracts with operational creditors for the supply of products and services. Combining financial and operational creditors equates to treating unequal’s alike and a breakdown of the categorization carefully formed by the Parliament.

Lastly, the promoters and guarantors were of the opinion that the guarantor’s obligation was co-extensive[4] with the corporate debtor’s, and if a resolution plan was approved, the personal guarantor’s responsibility would be extinguished as well. The petitioners relied on the decision in the case of Committee of Creditors of Essar Steel India Ltd. v. Satish Kumar Gupta[5] wherein the court observed that an approval of a resolution plan in respect of a corporate debtor amounted to the extinction of all outstanding claims against the debtor.

Supreme Court Judgment

The Supreme Court stated that it was clear that the mechanism used by the Central Government to implement certain provisions of the Act had a specific purpose: to achieve the IBC’s objectives in relation to the priorities. “The apex court said there was an intrinsic connection between personal guarantors and their corporate debtors and it was this “intimate” connection that made the government recognize personal guarantors as a “separate species” under the IBC.”[6]

According to the Hon’ble Supreme Court, there appeared to be compelling grounds why the forum for adjudicating insolvency processes should be common which should be through the NCLT. The NCLT would thus be able to look at the big picture, so to speak, of the nature of the assets available, whether during the corporate debtor’s insolvency proceedings or afterward. The Committee of Creditors would be better able to frame realistic resolution plans if they had a complete picture, keeping in mind the possibility of recovering some of the creditor’s dues from personal guarantors. Based on this discussion, the Court concluded that the contested notification was neither a legislative act nor an instance of improper and selective application of the IBC’s provisions.

The court also cleared up a misunderstanding among petitioners that acceptance of a resolution plan for corporate debtors would also discharge the personal guarantor’s obligations and said that The release or discharge of a principal borrower from his or her obligation by operation of law, or as a result of a liquidation or bankruptcy procedure, does not absolve the surety/guarantor of his or her duty arising from an independent contract. As a result, the Notification was found to be legal and valid, and the writ petitions, transferred cases, and transfer petitions in this case were all dismissed.

Analysis and aftermath

The government has started the procedure and currently offers a full solution for the Corporate Debtor’s CIRP as well as the individual who has supplied a guarantee for that Corporate Debtor. As a result, the gap or limitation in the IBC that had previously limited the adjudication of cases involving corporate guarantors solely has been lifted, and creditors will now be entitled to seek repayment from either of them, i.e. the Corporate Debtor or the Personal Guarantor of the Corporate Debtor. Though the obligations were always coextensive legally in accordance with established principles of law, MCA has now brought Corporate Debtor and Personal Guarantor into the same operational platform. Following that, such personal guarantors might file a claim for insolvency with NCLT.

This will be a significant boost because lenders will now be empowered to pursue funds from promoters/personal guarantors if the amount recovered from the Corporate Debtor is insufficient, and in cases where bankers initiate IBC procedures, they may have to re-evaluate the entire ground scenario. Though the development is exactly as expected, it may cause some anxiety among promoters, particularly those who are either facing IBC procedures (or are expecting to face IBC due to defaults) or who are likely to face IBC due to defaults. This may also force promoters to consider and strategize about the extent to which they might use their personal assets to obtain corporate financing.

Similarly, despite such notification, advisers’ jobs may not be easy due to unanswered questions such as how to handle dual legal cases; to what extent can a creditor collect money from a personal guarantor, and the practical challenges of pursuing both for recovery, among others. As a result, these issues may be presented in a court of law shortly, and the appropriate honorable courts will investigate these issues in accordance with the law and equity principles.

Conclusion

Many famous industrialists who are the promoters of debt-ridden enterprises would be concerned by the ruling but many creditors will breathe a sigh of relief as a result of the immediate judgement, which has opened the door to the personal guarantors’ asset pool under the IBC. Personal guarantors are more likely to “arrange” for the payment of the debt to the creditor bank in order to achieve a quick discharge if insolvency proceedings are filed against them.

Though only time will tell how such things develop and how honest courts administer justice, the government appears to be on the right track to achieve its goal of instilling financial discipline among borrowers, particularly corporate borrowers.

[1] Indian Contract act, 1872, Act No. 9, Section 126

[2] Vasu Dev Singh & Ors. v. Union of India & Ors., 2006 12 SCC 753.

[3] Swiss Ribbons (P.) Ltd. v. Union of India, 2019 4 SCC 17

[4] Kundanlal Dabriwala v. Haryana Financial Corporation, 2012 171 Comp Cas 94

[5] Committee of Creditors of Essar Steel India Ltd. v. Satish Kumar Gupta, 2019 SCC 1478

[6] Lalit Kumar Jain v. Union of India and Ors., Transfer Case (Civil) No. 245/2020

Written by: Aditya Sharma