Whatsapp

Whatsapp

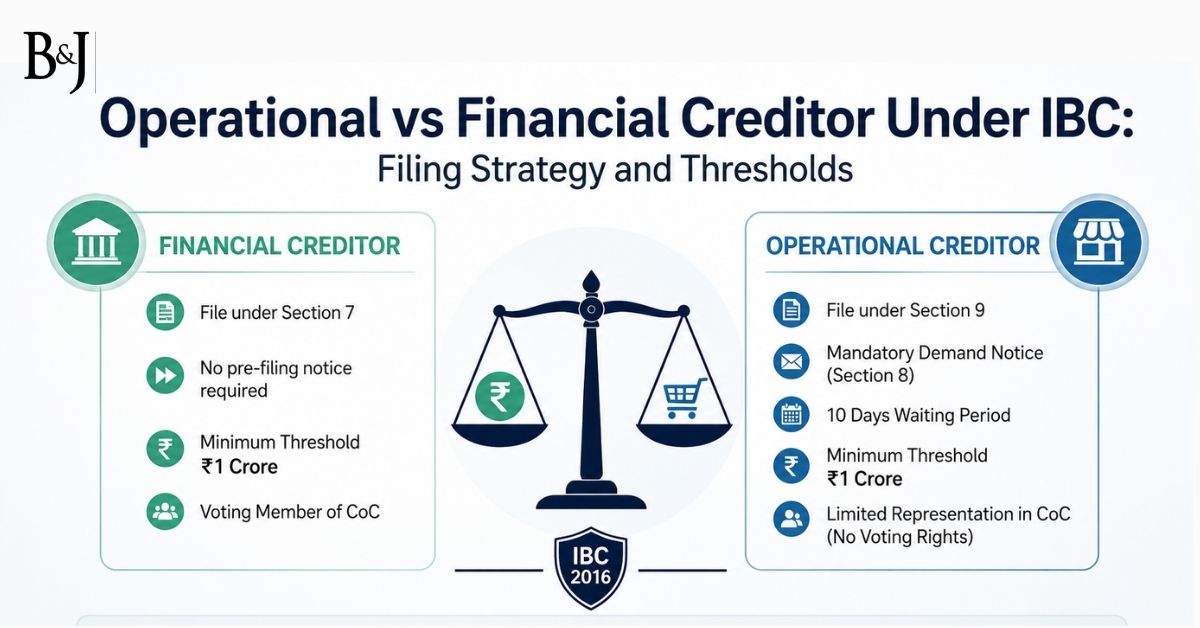

Operational vs Financial Creditor Under IBC: Filing Strategy and Thresholds

Executive Summary The distinction between an operational creditor and a financial creditor under the Insolvency and Bankruptcy Code, 2016 (“IBC” or “the Code̶

Personal Criminal Liability of Directors Under Section 138 NI Act Remains Unaffected by IBC Moratorium: Bombay High Court Ruling

Introduction The intersection of insolvency law and criminal liability has emerged as one of the most debated areas in contemporary Indian jurisprudence. The Bombay High Court̵

Threshold Limit Under IBC Section 9 for Initiating Insolvency: Clarification by NCLT Mumbai Bench

Introduction In a recent judgment, the NCLT Mumbai Bench has provided important clarifications regarding the applicability of the threshold limit for initiating corporate insolvenc

Pre-Packaged Insolvency Resolution Process (PPIRP): Unraveling Its Potential in the Realm of IBC

Introduction In recent years, the landscape of insolvency and bankruptcy resolution in India has undergone significant transformations, spurred by the enactment of the Insolvency a

Time Value of Money: Expanding the Horizon of Financial Debt with the NCLAT’s Verdict

Introduction In a landmark judgment delivered on 02.04.2024, the NCLAT provided crucial insights into the interpretation of financial debt under the Insolvency and Bankruptcy Code

Avoidance Transactions under IBC: Ensuring Accountability through the NCLT’s Directive

Introduction The NCLT Ahmedabad Bench’s judgment in *Mr. Shalabh Kumar Daga RP of Silver Proteins Pvt. Ltd. Vs. Mr. Himanshu J Domadia and Ors.* dated 11 March 2024, illumina

Financial Debt Under IBC: Navigating Interest-Free Loans Terrain with Insights from the Supreme Court

In a landmark decision, the Supreme Court of India, in the case of *M/s Orator Marketing Pvt. Ltd. vs. M/s Samtex Desinz Pvt. Ltd.*, delves into the intricacies of financial debt u

Commercial Wisdom of Committee of Creditors: Navigating Homebuyer Dissatisfaction in Insolvency Resolutions – Insights from NCLAT

The National Company Law Appellate Tribunal (NCLAT), New Delhi, recently delivered a significant judgment in the case involving Mr. Girish Nalavade against Bhrugesh Amin and Ors.,

Dissenting Financial Creditors under IBC: A Matter for Larger Bench Consideration

Introduction The Insolvency and Bankruptcy Code (IBC) has been a subject of intense legal scrutiny and interpretation in recent years. One of the most contentious issues pertains t

Decisions of Committee of Creditors to Liquidate under IBC: A NCLAT Judgment Analysis

Understanding the Role of Single Operational Creditor in CoC Under IBC and the Requirement of Reasoning for Liquidation The Insolvency and Bankruptcy Code, 2016 has fundamentally t