Whatsapp

Whatsapp

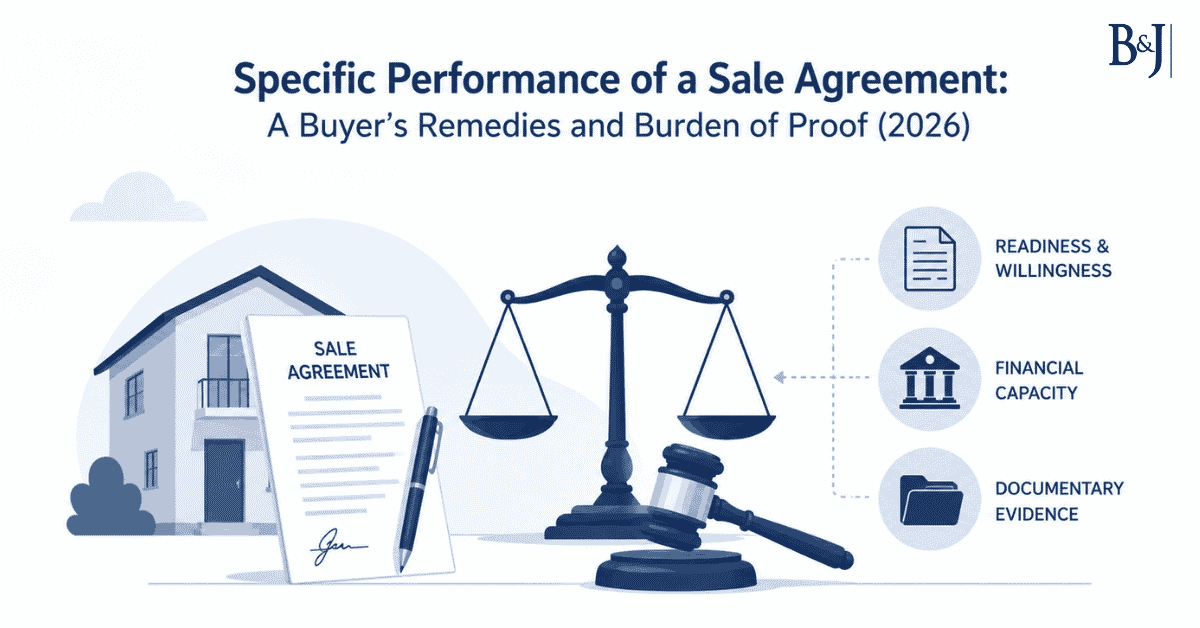

Specific Performance of a Sale Agreement: A Buyer’s Remedies and Burden of Proof (2026)

Executive Summary Specific performance sale agreement disputes constitute a significant portion of civil litigation in India involving immovable property. When a seller refuses to

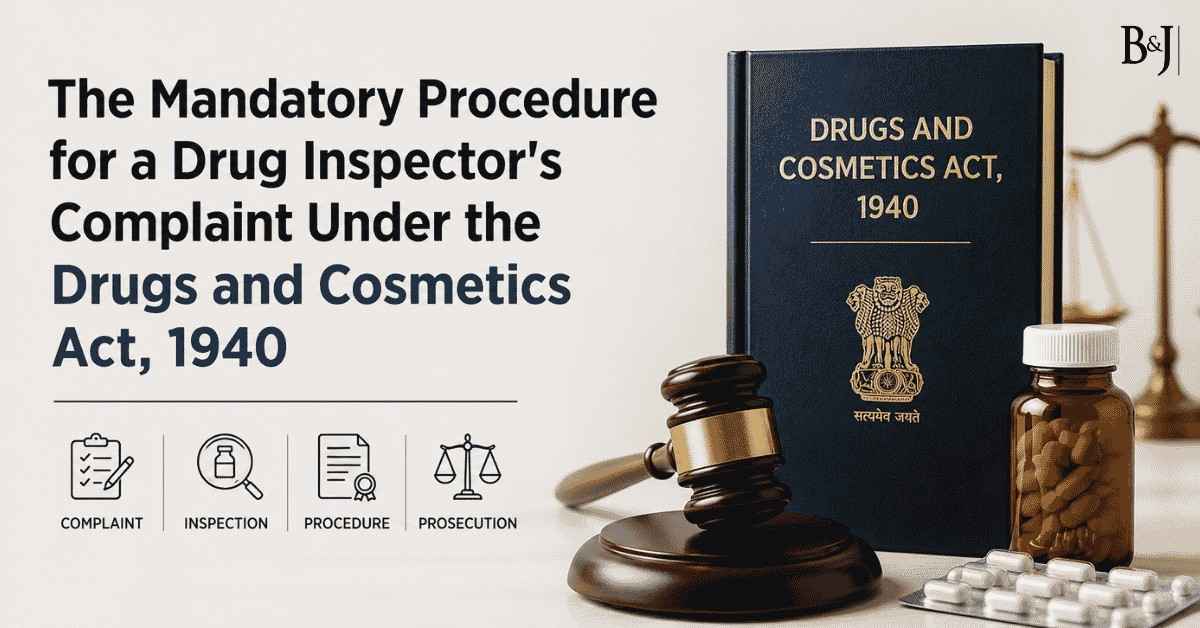

The Mandatory Procedure for a Drug Inspector’s Complaint Under the Drugs and Cosmetics Act, 1940

ABSTRACT The Drugs and Cosmetics Act, 1940 establishes a unique prosecution architecture: criminal proceedings for quality offences can be initiated only through a complaint, not t

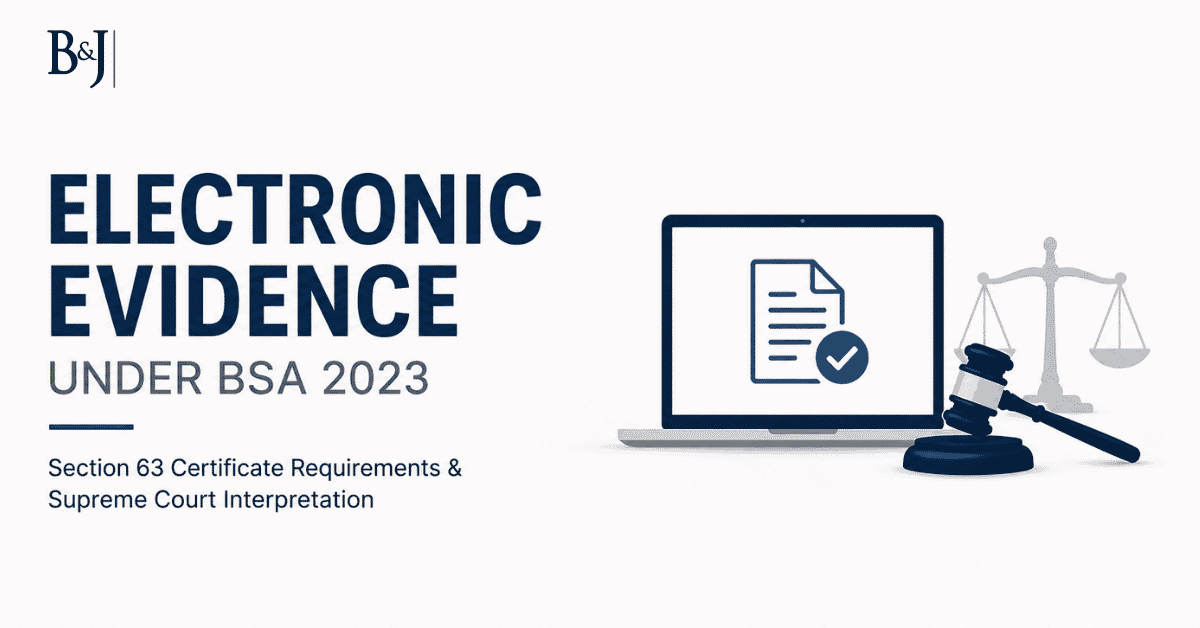

Electronic Evidence Under BSA 2023: Section 63 Certificate Requirements & Supreme Court Interpretation

Section 63 Certificate Requirements & Supreme Court Interpretation I. From Navjot Sandhu to Section 63 BSA, 2023: Evolution of Electronic Evidence Law The law governing electro

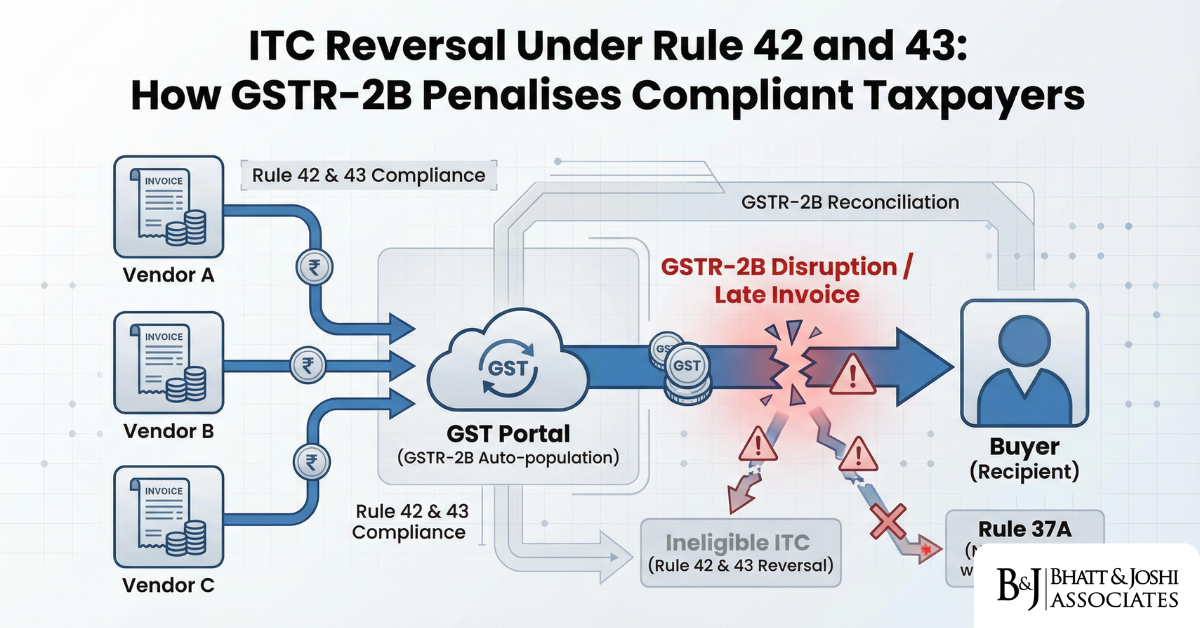

ITC Reversal Under Rule 42 and 43: Why the GSTR-2B Auto-Reversal Formula Penalises Compliant Taxpayers for Vendor Defaults

Introduction The Goods and Services Tax (GST) framework in India, introduced on 1 July 2017, was built on the promise of seamless Input Tax Credit (ITC) flow across the supply chai

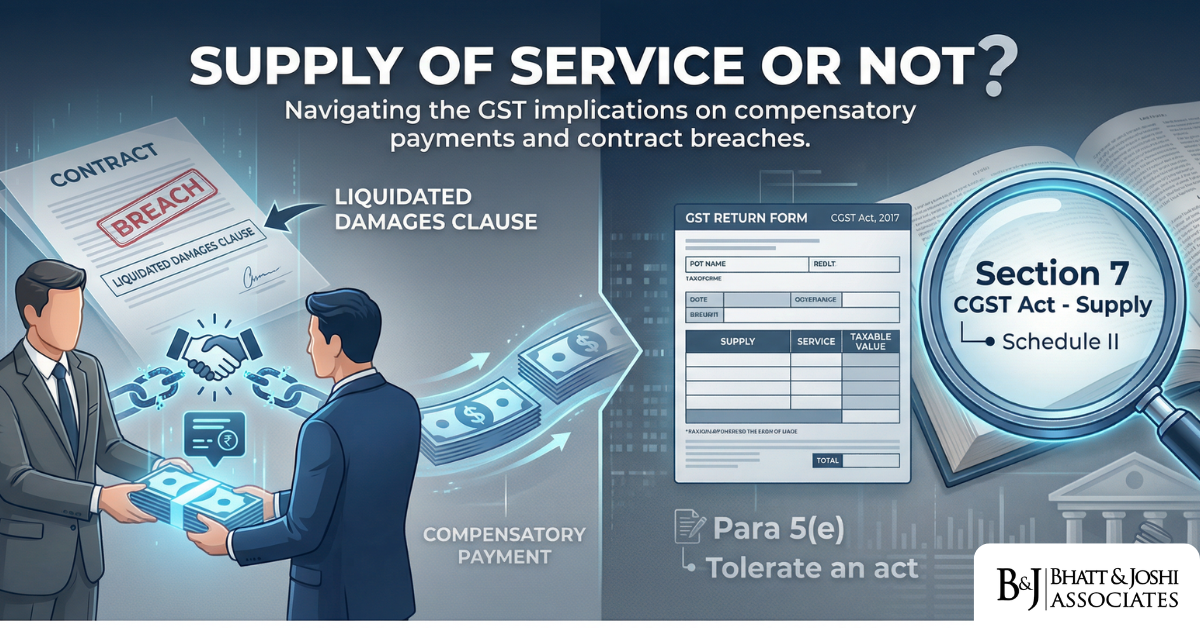

GST on Liquidated Damages: Supply of Service or Not? The Unsettled Jurisprudence After Safari Retreats

Introduction: Liquidated Damages and the Scope of “Supply” Under GST Few questions in Indian GST law have generated as much confusion at the field level as the one that seems d

The Applicability of Section 94 of the RFCTLARR Act, 2013 to Acquisitions under the Railways Act, 1989 for Infrastructure Intersections

Executive Summary The modernization of India’s infrastructure landscape frequently necessitates the intersection of linear projects, such as railway corridors crossing existi

Corporate Guarantees and Transfer Pricing – The Micro Ink Revolution

1. INTRODUCTION: THE GUARANTEE PRICING CONTROVERSY The Problem That Micro Ink Solved Pre-2016 Scenario: A multinational company (MNC) with Indian subsidiary structure: Parent compa

The Suo Moto Disallowance Trap – When Your Own Return Becomes Evidence Against You

1. INTRODUCTION: THE SELF-INCRIMINATION PARADOX The Core Tension There’s a peculiar paradox in Indian tax law: the more transparent and self-critical you are in your tax retu

The Satisfaction Note Doctrine in Income Tax Search Assessments: From Calcutta Knitwears to Jasjit Singh

A Comprehensive Legal Analysis of Procedural Safeguards, Judicial Safeguards, and Practical Implementation Under the Income Tax Act, 1961 Executive Summary: Key Takeaways on the Sa

Oil and Gas Land Rights: PNGRB Act, Pipeline ROW, and Exploration Licenses

Introduction India’s oil and gas sector operates within a complex legal framework that balances federal regulatory authority with state land rights, creating a multifaceted s