Whatsapp

Whatsapp

Harmonizing Land Acquisition Compensation across Special Acts: The 2015 Order and Tarsem Singh

For a landowner, the identity of the statute under which the land is taken ought to be a matter of i

Section 24(2) of the Land Acquisition Act: When Does an Acquisition Really Lapse?

When Parliament replaced the colonial Land Acquisition Act, 1894 with the Right to Fair Compensation

Severance & Injurious Affection — Forgotten Heads in Land Acquisition

Ask most landowners what they were paid for their acquired land and they will quote a single number:

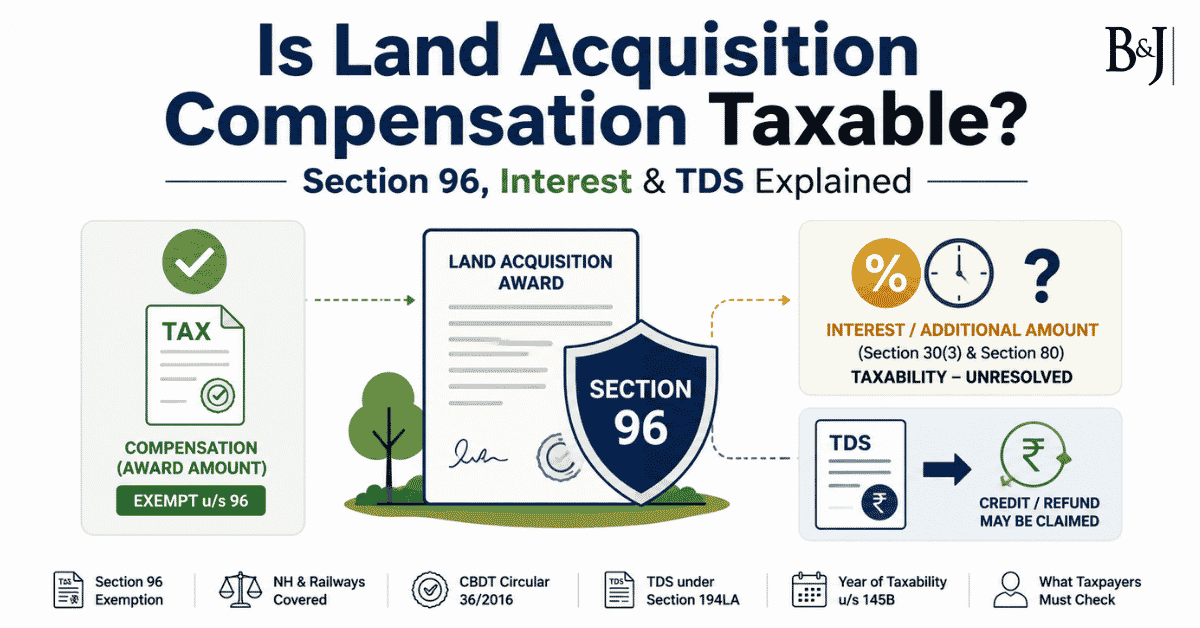

Is Land Acquisition Compensation Taxable? Section 96, Interest & TDS Explained

A landowner who has fought for a fair award often assumes that the enhanced amount finally received

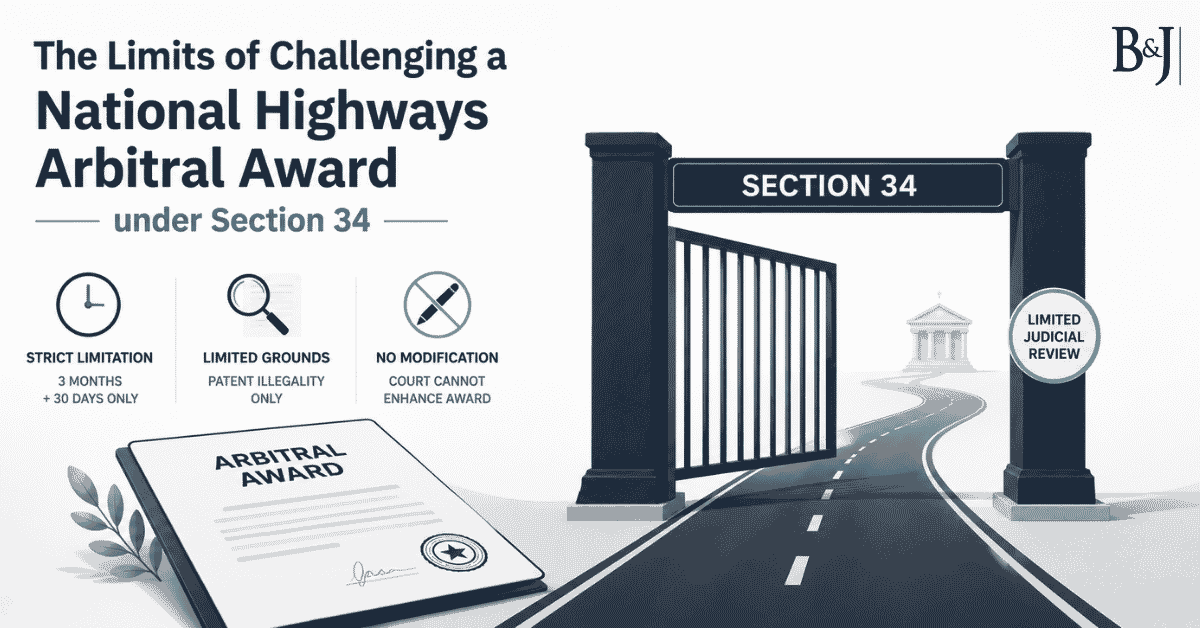

The Limits of Challenging a National Highways Arbitral Award under Section 34

When land is acquired for a National Highway, the landowner does not receive a court-determined comp

The Compensation Architecture of the LARR Act, 2013

Compensation under the Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitati

Three Forums for Land Acquisition Compensation Enhancement in India – s.64 Reference, NH Arbitration and the Railways Act

After the Removal of Difficulties Order of 2015 and the harmonisation that followed, a landowner acq

Determining Market Value in Land Acquisition: The Evidentiary Battleground

Every land acquisition compensation dispute, when stripped to its essentials, resolves into a single

Fair Compensation in Indian Land Acquisition: LARR, Railways and National Highways — A Practitioner’s Map

When the State takes a person’s land, the Constitution and statute promise something in return