Whatsapp

Whatsapp

Constitutional Validity of the Insolvency and Bankruptcy Code (IBC): A Legal Analysis

Introduction

The Insolvency and Bankruptcy Code, 2016 represents a watershed moment in India’s economic legislation, consolidating multiple fragmented laws into a unified framework for resolving corporate insolvency. Since its enactment on May 28, 2016, the Code has faced rigorous constitutional scrutiny through several landmark Supreme Court judgments. The constitutional validity of the IBC has been affirmed through judicial pronouncements that have examined its provisions against fundamental rights guaranteed under the Constitution of India, particularly Articles 14, 19(1)(g), and the doctrine of legislative competence. This article examines the regulatory framework, legislative intent, and judicial interpretation that have shaped the constitutional foundation of India’s insolvency regime.

Historical Context and Legislative Framework

Before the enactment of the Insolvency and Bankruptcy Code, India’s insolvency landscape was governed by a patchwork of legislations including the Sick Industrial Companies (Special Provisions) Act, 1985, the Recovery of Debts Due to Banks and Financial Institutions Act, 1993, and the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. These laws operated in silos, creating jurisdictional conflicts and prolonged litigation that failed to maximize asset value or facilitate timely resolution.

Recognizing these systemic failures, the Ministry of Finance constituted the Bankruptcy Legislative Reforms Committee in August 2014 under the chairmanship of T.K. Viswanathan. The Committee submitted its report along with a draft bill in November 2015, which formed the foundation for the current Code. The Code was introduced in the Lok Sabha on December 23, 2015, referred to a Joint Parliamentary Committee for detailed scrutiny, and subsequently passed by both Houses of Parliament in May 2016.

The Code establishes a time-bound process for resolving corporate insolvency, with the Corporate Insolvency Resolution Process required to be completed within 180 days, extendable by a maximum of 90 days. The adjudicatory framework is vested in the National Company Law Tribunal for corporate persons and the Debt Recovery Tribunal for individuals and partnership firms. The Code also created institutional infrastructure including the Insolvency and Bankruptcy Board of India, insolvency professionals, and information utilities to facilitate the resolution process.

Foundational Judicial Pronouncements

The Innoventive Industries Precedent

The first comprehensive judicial examination of the IBC constitutional validity emerged in Innoventive Industries Ltd. v. ICICI Bank & Anr., decided by the Supreme Court on August 31, 2017 [1]. This case marked a paradigm shift in India’s insolvency jurisprudence, establishing foundational principles that would guide subsequent interpretations.

In Innoventive Industries, the corporate debtor challenged the admission of an insolvency petition filed by ICICI Bank under Section 7 of the Code. The debtor argued that notifications issued under the Maharashtra Relief Undertakings (Special Provisions) Act, 1958 had suspended its liabilities, and therefore no debt was legally due. The Supreme Court rejected this contention, holding that the Code, being a later Parliamentary enactment with an overriding non-obstante clause under Section 238, would prevail over conflicting State legislation.

The judgment clarified several critical aspects of the Code’s operation. First, it defined “default” under Section 3(12) as the non-payment of a debt once it becomes due and payable, including non-payment of even a part thereof or an installment amount. The Court emphasized that the existence of a dispute regarding the debt does not prevent the initiation of insolvency proceedings, as long as the debt is legally due. Second, the judgment addressed the issue of locus standi, holding that once an insolvency professional is appointed to manage the company, erstwhile directors lose their authority to file appeals on behalf of the corporate debtor.

Most significantly, the Court articulated the legislative philosophy underlying the Code, stating that it represents a fundamental shift from debtor-in-possession to creditor-in-control regime. Unlike the United States Bankruptcy Code where the debtor remains in possession, the Indian framework divests the erstwhile management of its powers and vests them in a professional agency to continue the business as a going concern until a resolution plan is drawn up. The Court noted that the scheme is designed to revive the corporate debtor and restore it to financial health, with liquidation being a measure of last resort.

Swiss Ribbons and the Comprehensive Constitutional Challenge

The most exhaustive examination of the Code’s constitutional validity came in Swiss Ribbons Pvt. Ltd. & Anr. v. Union of India & Ors., decided on January 25, 2019 [2]. This watershed judgment addressed multiple constitutional challenges to various provisions of the Code, ultimately upholding its validity in its entirety while providing detailed reasoning on each contested provision.

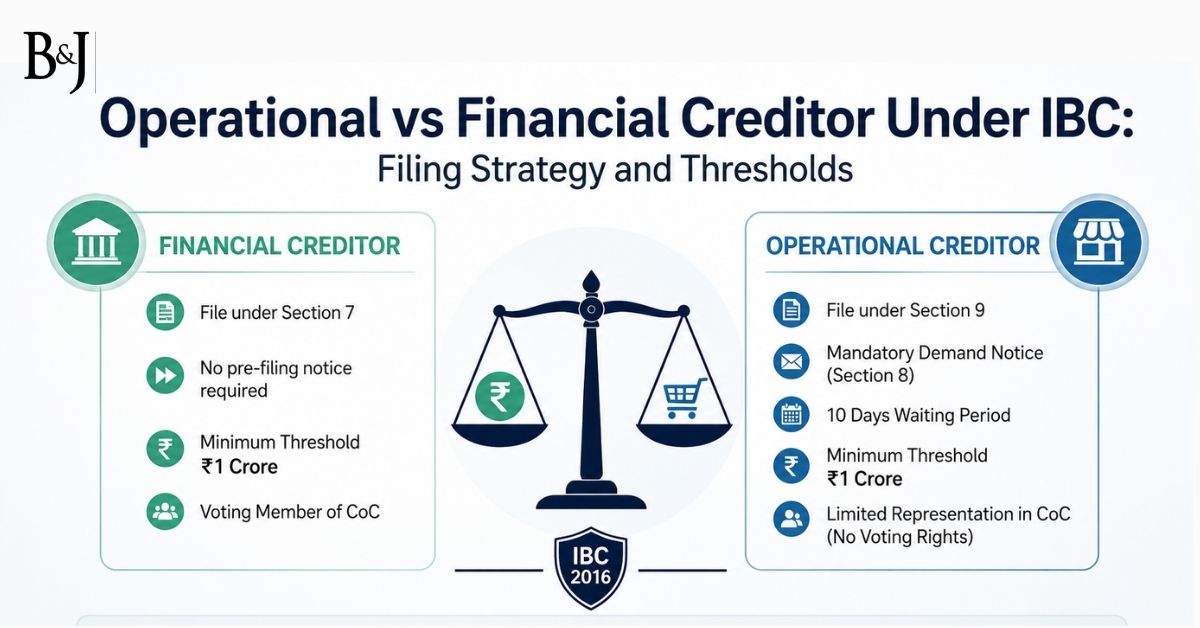

The petitioners in Swiss Ribbons raised several grounds challenging the constitutionality of the Code. They contended that the classification between financial creditors and operational creditors was discriminatory and violated Article 14 of the Constitution. They argued that operational creditors, despite being creditors with legitimate claims, were denied voting rights in the Committee of Creditors, which comprised only financial creditors. This differential treatment, according to the petitioners, lacked any intelligible differentia and had no rational nexus with the object sought to be achieved.

The Supreme Court rejected these contentions, holding that the distinction between financial creditors and operational creditors was based on sound commercial rationale. Financial creditors, the Court observed, assess the viability and feasibility of the corporate debtor before extending credit and continue to monitor the debtor’s financial health throughout the loan tenure. They have specialized personnel and resources to evaluate resolution plans and determine the best course of action for reviving the corporate debtor. Operational creditors, on the other hand, provide goods or services in the ordinary course of business and generally do not possess the same level of financial expertise or long-term engagement with the debtor’s business operations.

The Court emphasized that the Code does not discriminate against operational creditors in terms of their right to initiate insolvency proceedings. Both financial creditors under Section 7 and operational creditors under Sections 8 and 9 can trigger the Corporate Insolvency Resolution Process. The differentiation lies only in the composition of the Committee of Creditors and voting rights, which is justified by the distinct nature of their relationship with the corporate debtor.

The judgment also addressed challenges to Section 29A, which specifies categories of persons ineligible to submit resolution plans. The petitioners argued that this provision was retrospective in application and impaired vested rights of erstwhile promoters to participate in the resolution process. The Court held that Section 29A is not retrospective merely because some of the eligibility criteria refer to past events or conduct. The provision creates prospective ineligibility based on certain past circumstances, which is permissible under constitutional law. The Court further noted that resolution applicants have no vested right to be considered in the resolution process, and therefore Section 29A does not violate any pre-existing legal entitlement.

Regarding Section 12A, which permits withdrawal of insolvency applications with the approval of 90% of the Committee of Creditors, the petitioners challenged the high threshold as arbitrary. The Court rejected this challenge, explaining that the high threshold ensures that all financial creditors collectively agree to the withdrawal, as ideally an omnibus settlement involving all creditors should be entered into. The Court also noted that the National Company Law Tribunal and the National Company Law Appellate Tribunal retain jurisdiction under Section 60 to set aside arbitrary rejections of withdrawal applications by the Committee of Creditors.

The Swiss Ribbons judgment also examined the constitutional validity of the tribunals established under the IBC. The petitioners contended that members of the National Company Law Tribunal and National Company Law Appellate Tribunal had been appointed contrary to the Supreme Court’s judgment in Madras Bar Association v. Union of India. The Court found that the appointments were made in compliance with the Madras Bar Association directives, with a properly constituted Selection Committee comprising judicial members and government representatives. However, the Court directed the Union of India to establish circuit benches of the National Company Law Appellate Tribunal within six months and to transfer administrative support for all tribunals to the Ministry of Law and Justice.

The Essar Steel Judgment and Further Validation

The constitutional validity of amendments to the IBC was further tested in Committee of Creditors of Essar Steel India Limited v. Satish Kumar Gupta & Ors., decided on November 15, 2019 [3]. This case arose from the insolvency resolution of Essar Steel India Limited, where the National Company Law Appellate Tribunal had directed equal distribution of funds between financial and operational creditors, setting aside the resolution plan approved by the Committee of Creditors.

The Supreme Court set aside the National Company Law Appellate Tribunal’s judgment and upheld the constitutional validity of the Insolvency and Bankruptcy Code (Amendment) Act, 2019. The Court reiterated that the Committee of Creditors, comprising financial creditors, is best positioned to assess the viability of resolution plans based on their commercial wisdom. The Court held that the Code differentiates between financial creditors and operational creditors, as well as between secured and unsecured creditors, and these distinctions are constitutionally valid.

The judgment clarified that the principle of equality enshrined in Article 14 requires only that equals be treated equally, not that all creditors receive proportionate payments regardless of their status or security interests. The Court observed that requiring equal treatment of all creditors would disincentivize secured financial creditors from supporting resolution plans, as they would receive better recoveries in liquidation. This would defeat the primary objective of the Code, which is to revive corporate debtors rather than liquidate them.

The Essar Steel judgment also addressed the fair and equitable treatment of operational creditors. The Court interpreted the amended Regulation 38 of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016, as requiring resolution plans to explain how they have dealt with the interests of operational creditors, not necessarily requiring equal monetary distribution. This interpretation balanced the rights of operational creditors with the commercial realities of insolvency resolution.

Personal Guarantors and Constitutional Validity

The constitutional validity of provisions relating to personal guarantors was examined in Dilip B. Jiwrajka v. Union of India & Ors., decided on November 9, 2023 [4]. This case involved 384 writ petitions challenging Sections 95 to 100 of the Code, which govern the insolvency resolution process for personal guarantors to corporate debtors.

The petitioners contended that these provisions violated the principles of natural justice by condemning personal guarantors unheard and vesting unfettered powers in Resolution Professionals. They also argued that the provisions violated the fundamental right to privacy by allowing Resolution Professionals to requisition private financial records without first establishing the validity of the debt and default.

The Supreme Court upheld the constitutional validity of these provisions, holding that the Code provides adequate safeguards and opportunities for personal guarantors to present their case. The Court noted that the insolvency resolution process for personal guarantors mirrors the process for corporate debtors, with appropriate modifications. The interim moratorium under Section 96 protects the interests of personal guarantors during the resolution process, while ensuring that creditors can pursue recovery in a time-bound manner.

On the privacy concerns, the Court referenced the landmark judgment in K.S. Puttaswamy v. Union of India [5], acknowledging that while privacy is a fundamental right, it is subject to reasonable restrictions. The Court held that the Code’s framework justifiably mandates the collection of financial information by Resolution Professionals to ascertain the validity of debts and defaults, ensuring a thorough and fair resolution process. The power to access financial information is not unfettered but is exercised under the supervision of the Debt Recovery Tribunal.

Regulatory Framework and Institutional Architecture

The Insolvency and Bankruptcy Code establishes a robust regulatory framework administered by the Insolvency and Bankruptcy Board of India, a regulatory body established under Section 188 of the Code. The Board is responsible for regulating insolvency professionals, insolvency professional agencies, and information utilities. It also exercises regulatory oversight over the conduct of insolvency resolution processes and lays down standards for insolvency professionals.

The Code empowers the Board to make regulations on various aspects of the insolvency resolution process. Key regulations include the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) Regulations, 2016, which prescribe detailed procedures for conducting Corporate Insolvency Resolution Process, the Insolvency and Bankruptcy Board of India (Liquidation Process) Regulations, 2016, and the Insolvency and Bankruptcy Board of India (Insolvency Professionals) Regulations, 2016.

The adjudicatory framework under the Code vests jurisdiction in specialized tribunals. For corporate persons, the National Company Law Tribunal exercises jurisdiction as the Adjudicating Authority under Section 60. Appeals from the National Company Law Tribunal lie to the National Company Law Appellate Tribunal under Section 61. For individuals and partnership firms, the Debt Recovery Tribunal serves as the Adjudicating Authority, with appeals lying to the Debt Recovery Appellate Tribunal. Further appeals on substantial questions of law lie to the Supreme Court under Section 62.

Comparative Analysis with International Frameworks

The Insolvency and Bankruptcy Code draws inspiration from international insolvency frameworks, particularly the United Kingdom Insolvency Act, 1986, and the United States Bankruptcy Code. However, it incorporates several distinctive features tailored to India’s economic and legal context.

Unlike the United States model where the debtor remains in possession under Chapter 11 bankruptcy proceedings, the Indian Code adopts a creditor-in-control approach where the management is vested in an insolvency professional. This feature is more aligned with the United Kingdom model, which the Supreme Court in Innoventive Industries noted as the primary influence on the Code’s design.

The Code’s emphasis on time-bound resolution distinguishes it from many international frameworks. The mandatory timelines for completing the Corporate Insolvency Resolution Process, though subject to some flexibility as clarified in the Essar Steel judgment, reflect the legislative intent to prevent value erosion through prolonged proceedings. This aspect addresses one of the primary failures of previous Indian insolvency laws, which allowed proceedings to drag on for years without definitive resolution.

Conclusion

The constitutional validity of the Insolvency and Bankruptcy Code (IBC) has been firmly established through extensive judicial scrutiny. The Supreme Court’s pronouncements in Innoventive Industries, Swiss Ribbons, Essar Steel, and Dilip B. Jiwrajka have validated the Code’s legislative framework, regulatory architecture, and procedural mechanisms. These judgments have recognized that the Code represents a legitimate exercise of legislative power to address the economic imperative of timely insolvency resolution while balancing the interests of all stakeholders.

The Code’s classification of creditors, the composition of the Committee of Creditors, the ineligibility criteria for resolution applicants, and the provisions governing personal guarantors have all withstood constitutional challenge. The courts have consistently emphasized that the Code is primarily a resolution and revival mechanism, not merely a recovery tool for creditors. This judicial endorsement has provided certainty to stakeholders and facilitated the Code’s implementation as a transformative economic legislation.

As the IBC continues to evolve through amendments and judicial interpretation, its constitutional validity remains secure. The framework demonstrates the judiciary’s deference to legislative policy in economic regulation while ensuring that fundamental constitutional principles are respected. The IBC stands as a testament to India’s commitment to creating a robust, time-bound, and creditor-friendly insolvency regime that balances competing interests and promotes economic efficiency.

References

[1] Innoventive Industries Ltd. v. ICICI Bank & Anr., Civil Appeal Nos. 8337-8338 of 2017, Supreme Court of India (August 31, 2017). Available at: https://indiankanoon.org/doc/181931435/

[2] Swiss Ribbons Pvt. Ltd. & Anr. v. Union of India & Ors., Writ Petition (Civil) No. 99 of 2018, Supreme Court of India (January 25, 2019). Available at: https://indiankanoon.org/doc/17372683/

[3] Committee of Creditors of Essar Steel India Limited v. Satish Kumar Gupta & Ors., Civil Appeal No. 8766-67 of 2019, Supreme Court of India (November 15, 2019). Available at: https://indiankanoon.org/doc/7427609/

[4] Supreme Court Upholds IBC Provisions on Personal Guarantors, Dilip B. Jiwrajka v. Union of India & Ors., Supreme Court of India (November 9, 2023). Available at: https://www.livelaw.in/law-firms/law-firm-articles-/supreme-court-personal-guarantors-ibc-presidency-towns-insolvency-act-cirp-nclat-resolution-professional-248885

[5] K.S. Puttaswamy v. Union of India, (2017) 10 SCC 1, Supreme Court of India.

[6] Supreme Court Upholds Validity of Insolvency & Bankruptcy Code, LiveLaw (January 15, 2022). Available at: https://www.livelaw.in/top-stories/supreme-court-validity-of-insolvency-bankruptcy-code-142379

[7] Insolvency and Bankruptcy Code is Constitutionally Valid: SC, Lexology (February 1, 2019). Available at: https://www.lexology.com/library/detail.aspx?g=a6ffcf59-2c18-4f9a-b04f-ad16e1eb67ea

[8] Challenge to the Constitutional Validity of the Insolvency and Bankruptcy Code, 2016: What the Supreme Court Held, Bar & Bench (February 21, 2019). Available at: https://www.barandbench.com/columns/supreme-court-constitutional-validity-ibc-2016

[9] Essar Steel India Limited: Supreme Court Reinforces Primacy of Creditors Committee in Insolvency Resolution, Cyril Amarchand Mangaldas (November 2019). Available at: https://corporate.cyrilamarchandblogs.com/2019/11/essar-steel-india-limited-supreme-court-reinforces-primacy-of-creditors-committee-insolvency-resolution/

Advocate Aaditya Bhatt

Senior Standing Counsel Income Tax Department, Advocate Gujarat High Court. Aaditya combines his technical and legal expertise to deliver strategic counsel in litigation, constitutional, and regulatory matters. He represents clients before High Courts and Tribunals with a technology-driven approach.