Whatsapp

Whatsapp

Can Appellate Court Criticism Demoralise Judges? Judicial Independence and the Chilling Effect

Introduction On 13 February 2026, Justice Pankaj Bhatia of the Allahabad High Court made a remarkabl

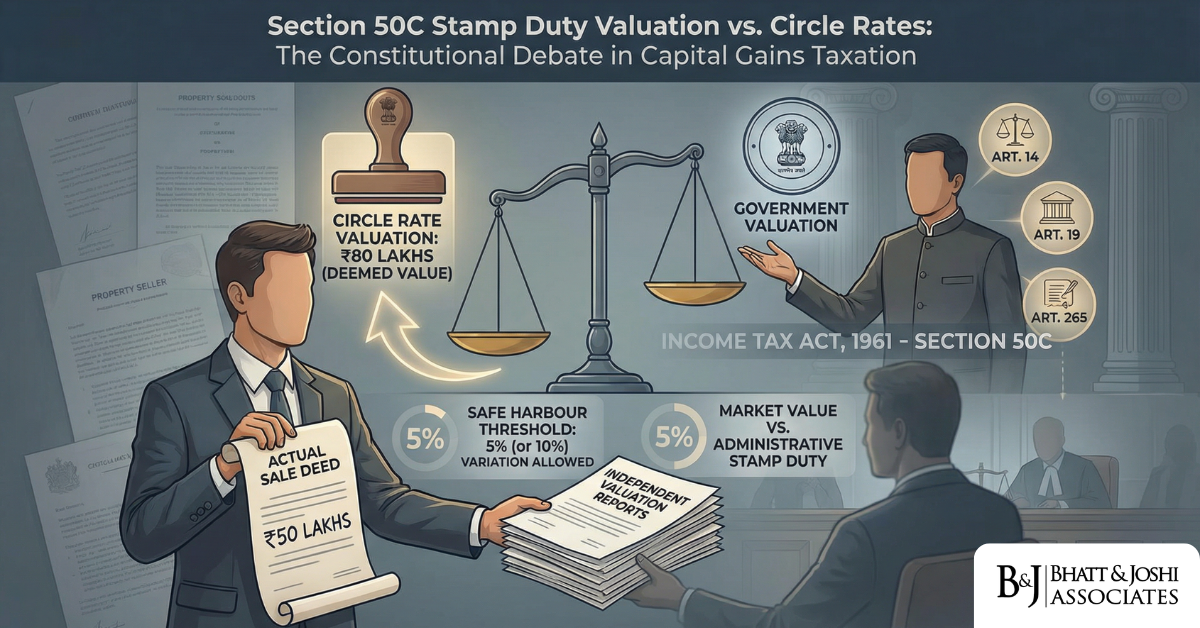

Section 50C of the Income Tax Act, 1961 Stamp Duty Valuation vs. Circle Rates: The Constitutional Validity of Deeming Fictions in Capital Gains

Introduction Few provisions in Indian income tax law generate as much sustained controversy, litigat

Livestream Donations and the TDS Gap on Creator Income in India: Why Streamers and Influencers Have No Withholding

Introduction India’s creator economy has grown into a multi-billion-rupee ecosystem, where gam

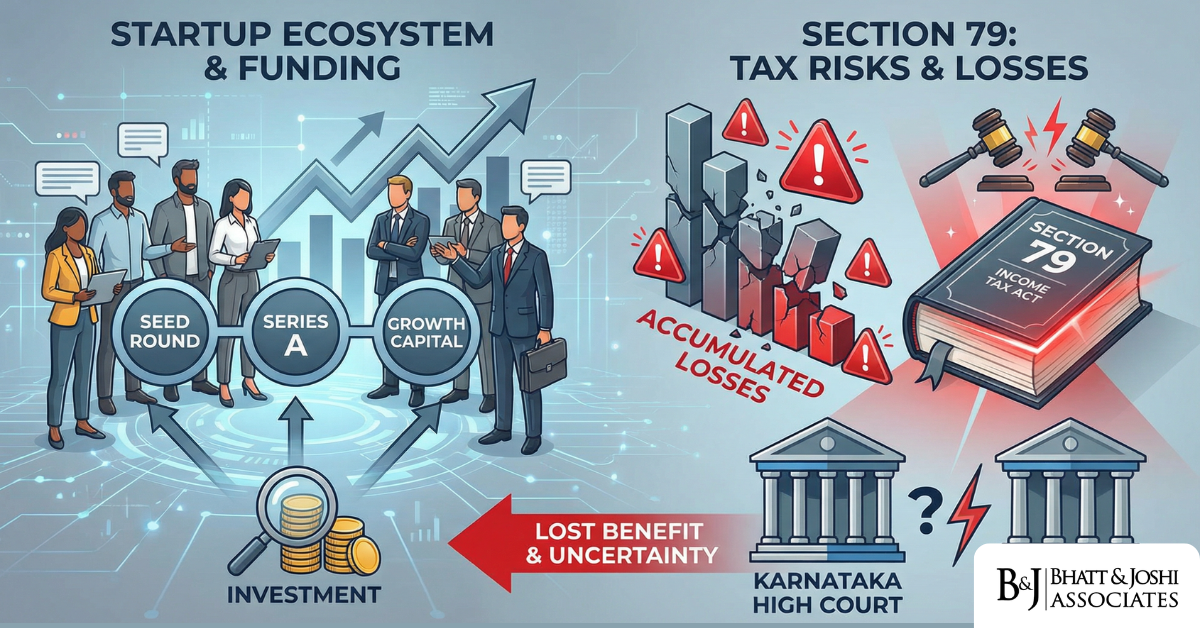

Startup Losses and Section 79 of the Income Tax Act, 1961: When Anti-Abuse Rules Kill Legitimate Restructuring

Introduction India’s startup ecosystem has grown into one of the most dynamic in the world, ye

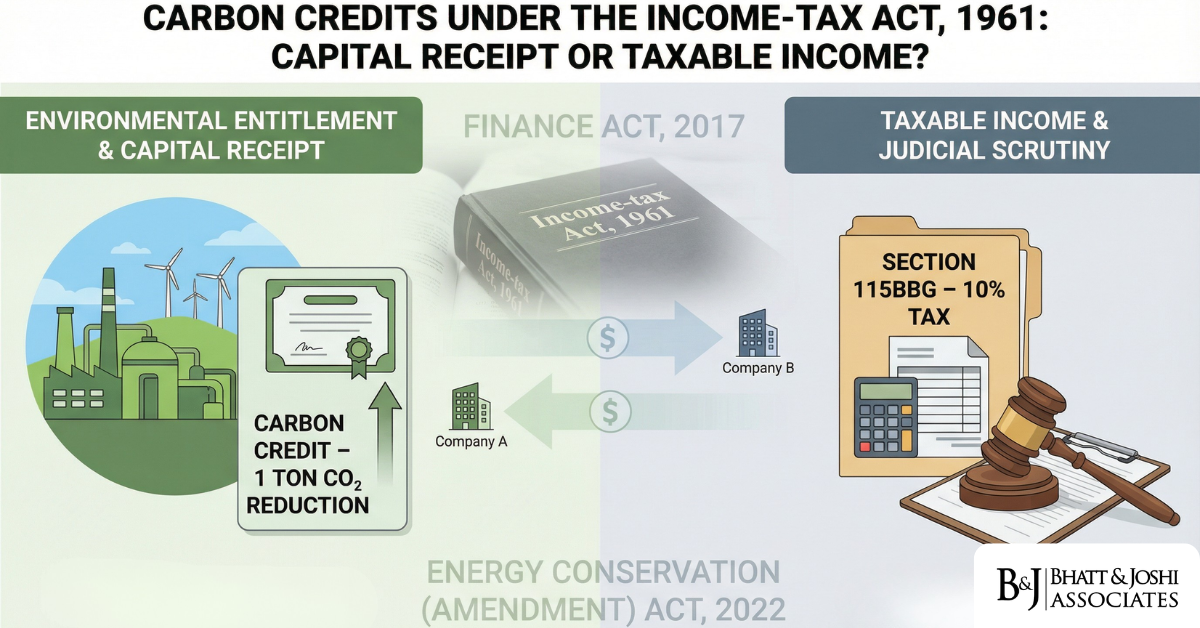

Income Tax Treatment of Carbon Credits: Asset, Income, or Capital Receipt Under the IT Act, 1961?

Introduction Carbon credits — formally known as Certified Emission Reductions (CERs) — have occu

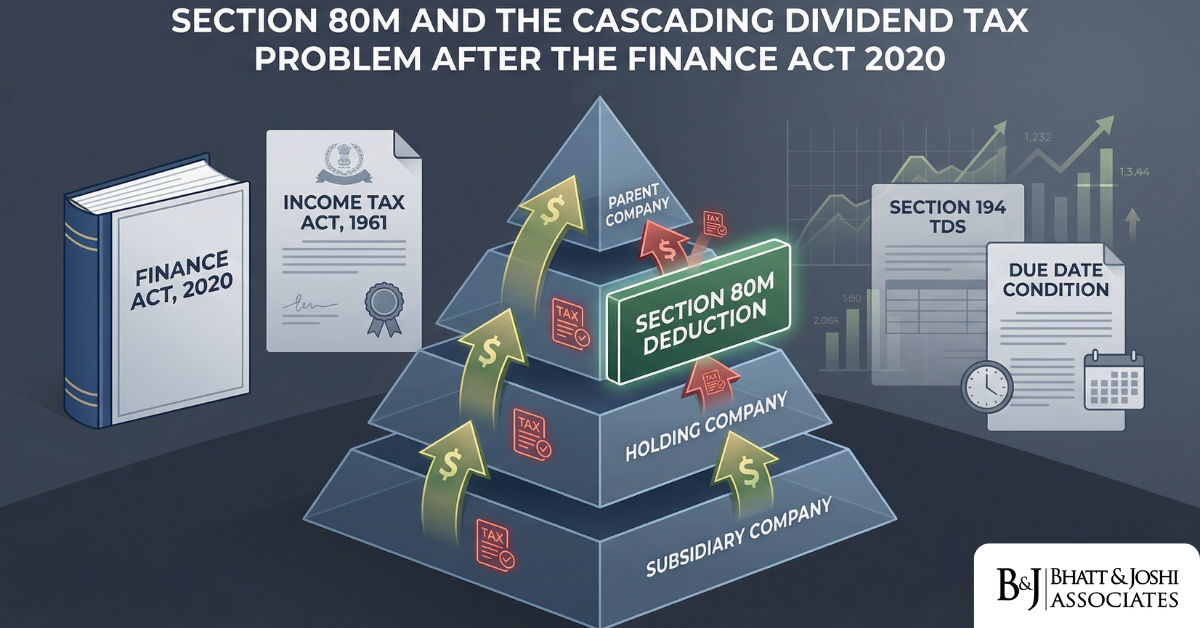

Section 80M Inter-Corporate Dividend Deduction: The Cascading Tax Problem the Finance Act 2020 Left Unresolved

Introduction When the Finance Act 2020 abolished the Dividend Distribution Tax (DDT) under Section 1

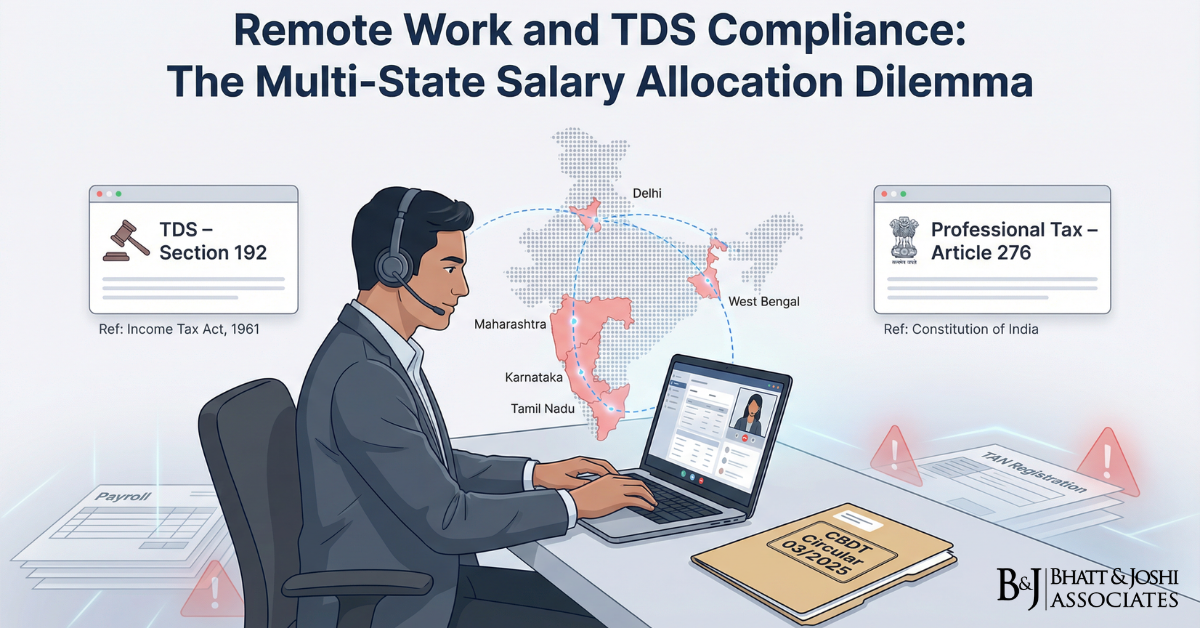

TDS on Salary for Remote Employees Across Multiple Indian States Under Section 192: Compliance Challenges”

Introduction The rise of remote work in post-pandemic India has created a TDS on salary compliance c

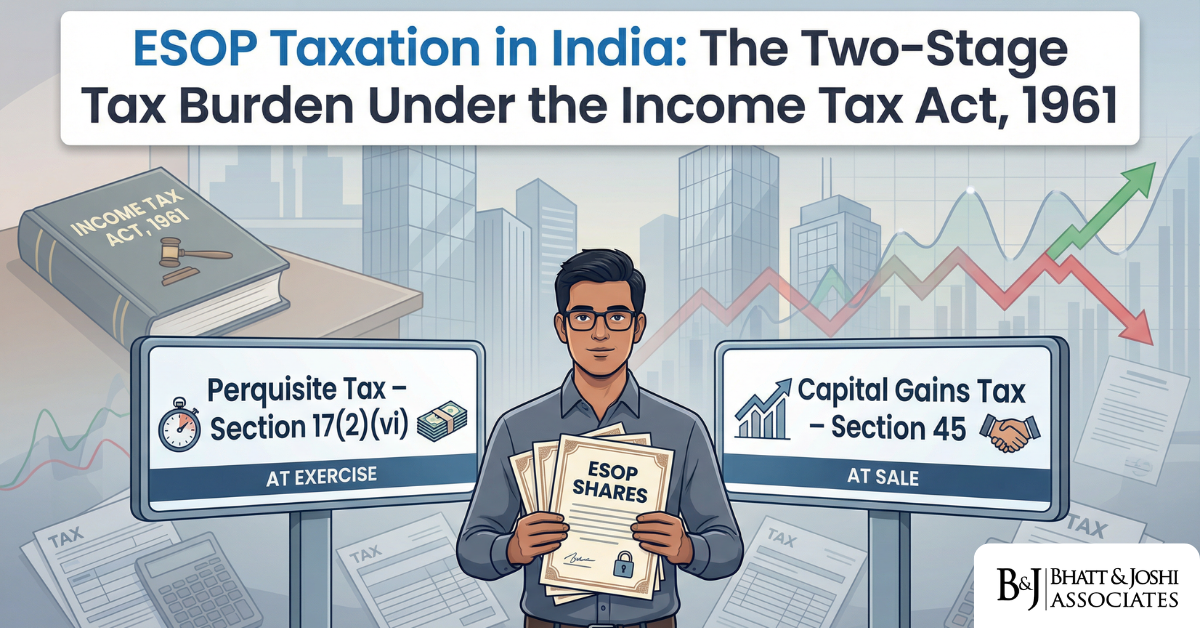

ESOP Taxation After Exit: Why Perquisite Tax at Exercise and Capital Gains at Sale Creates Double Taxation by Stealth

Introduction Employee Stock Option Plans (ESOPs) are among the most powerful instruments that Indian

Crypto Losses Under Section 115BBH: Why the No-Set-Off Rule Creates an Unconstitutional Tax on Notional Gains

Introduction When the Finance Act, 2022 introduced Section 115BBH into the Income Tax Act, 1961, it