Whatsapp

Whatsapp

Income Tax Treatment of Carbon Credits: Asset, Income, or Capital Receipt Under the IT Act, 1961?

Introduction

Carbon credits — formally known as Certified Emission Reductions (CERs) — have occupied an increasingly contentious space in Indian tax jurisprudence over the past two decades. As an internationally recognised tradeable commodity under the Kyoto Protocol, a single carbon credit represents the verified reduction of one tonne of carbon dioxide or an equivalent greenhouse gas (GHG) emission. While the environmental rationale behind these instruments is well understood, their precise character under the Income-tax Act, 1961 (the “IT Act”) has been the subject of considerable dispute between taxpayers and the Income-tax Department. The central question — whether proceeds from the transfer of carbon credits constitute a capital receipt, a revenue receipt, or business income — carries profound tax consequences and has shaped India’s evolving regulatory posture toward emission trading markets [1].

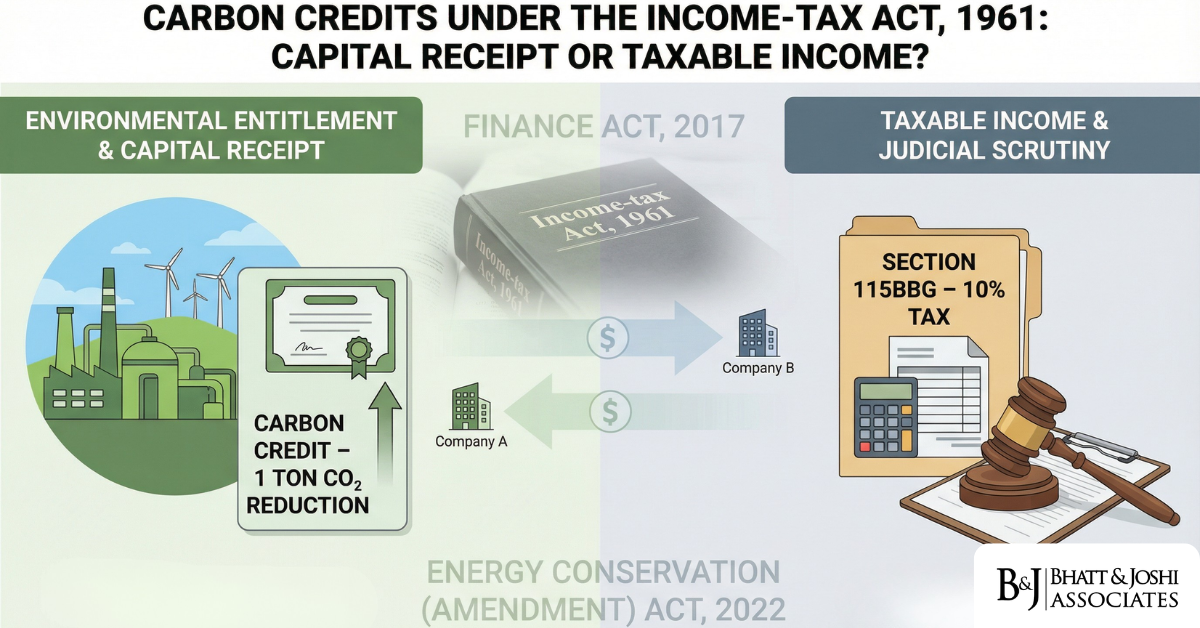

The fundamental distinction in Indian income tax law is this: revenue receipts are taxable unless specifically exempted, while capital receipts are not taxable unless a specific charging provision brings them within the scope of income. This binary has defined every judicial and legislative intervention on the carbon credit question, culminating in the insertion of Section 115BBG into the IT Act by the Finance Act, 2017, operative from Assessment Year 2018-19 onwards. Even so, the legal controversy has not fully settled, and the matter in Principal Commissioner of Income Tax v. Lanco Tanjore Power Co. Ltd. remains pending before the Supreme Court of India, demonstrating that the final word has not yet been pronounced [2].

What Are Carbon Credits and How Are They Generated?

Under the United Nations Framework Convention on Climate Change (UNFCCC) and the Kyoto Protocol, industrialised countries committed to reducing their GHG emissions. The Clean Development Mechanism (CDM) is one of the market-based tools under the Protocol that allows developed-country entities to invest in emission-reduction projects in developing countries, including India, in exchange for CERs. Entities that achieve emission reductions below their baseline are issued these credits, which can then be sold to entities that have exceeded their permitted limits.

Critically, a carbon credit is not generated as a product or by-product of the taxpayer’s manufacturing or service operations. It arises entirely from the quantified reduction of atmospheric pollution — an act validated by the UNFCCC — rather than from the taxpayer’s normal course of business. This fundamental characteristic has been central to the argument that carbon credits partake of the nature of a capital entitlement, not a trading commodity. As the ITAT, Hyderabad Bench, held in its landmark decision in My Home Power Ltd. v. DCIT [ITA No. 1114/Hyd/2009, dated 02.11.2012], carbon credit is “in the nature of an entitlement received to improve world atmosphere and environment reducing carbon, heat and gas emissions” [3].

The Revenue’s Position: Business Income or Revenue Receipt

From the very first assessments involving CERs, the Income-tax Department took the position that proceeds from the sale of carbon credits were taxable as business income under the head “Profits and gains of business or profession” under Sections 28 and 2(24) of the IT Act. The Department’s reasoning rested on the premise that carbon credits were earned in the course of the assessee’s business operations — for instance, by switching fuel sources or using renewable energy — and that because they had a recognised market and were quoted on stock exchanges, they were akin to trading stock and therefore a revenue receipt.

The Assessing Officers further leaned on Section 28(iv) read with Section 2(24)(vd) of the IT Act, which brings to tax “the value of any benefit or perquisite arising from business or exercise of profession.” Since the carbon credit was received in the context of a business enterprise, the Revenue argued it fell squarely within this definition. The Cochin Bench of the ITAT, in Apollo Tyres Ltd. v. ACIT [(2014) 47 taxmann.com 416 (Cochin-Trib.)], sided with the Revenue on this basis, holding that CERs were obtained in the course of business activity and that income on their sale was a benefit arising out of business under Section 28(iv) [4]. This remains the strongest judicial articulation of the Revenue’s position, though it has not been widely followed by other benches or by any High Court.

The Assessee’s Position and the Weight of Judicial Authority: Capital Receipt

The overwhelming weight of judicial authority — beginning with the ITAT and confirmed by multiple High Courts — has held that sale proceeds of carbon credits are capital receipts not liable to tax under any head of income under the IT Act. The foundational reasoning was laid down in My Home Power Ltd. v. DCIT (supra), where the ITAT, Hyderabad, reasoned that carbon credits are not an offshoot of business but an offshoot of “world concern” regarding the environment. The Tribunal held: “Carbon credit is not generated or created due to carrying on business but it is accrued due to world concern. The source of carbon credit is world concern and environment. The amount received for carbon credits has no element of profit or gain and it cannot be subjected to tax in any manner under any head of income. It is not liable for tax for the assessment year under consideration in terms of sections 2(24), 28, 45 and 56 of the Income-tax Act, 1961.” [3]

The Tribunal further held that CERs are not “capital assets” within Section 2(14), and accordingly their transfer cannot give rise to capital gains under Section 45. The reason is that carbon credits carry no cost of acquisition, and the computation mechanism under Section 48 fails in their case. There is thus no head of income — whether business profits, capital gains, or income from other sources — under which CER proceeds can be brought to charge.

This view was confirmed by the Andhra Pradesh High Court in Commissioner of Income Tax v. My Home Power Ltd. [ITAT Appeal No. 60 of 2014, dated 19.02.2014], where the Division Bench held: “Carbon Credit is not an offshoot of business but an offshoot of environmental concerns. No asset is generated in the course of business but it is generated due to environmental concerns. The Carbon Credit is not even directly linked with power generation.” The High Court affirmed that the receipt was correctly classified as a capital receipt not liable to tax [3].

The Karnataka High Court followed suit in CIT v. Subhash Kabini Power Corporation Ltd. [(2016) 385 ITR 592 (Karn.)], explicitly endorsing the Andhra Pradesh High Court’s analysis [4]. The Madras High Court, in CIT v. Wescare (India) Ltd. [Tax Case Appeal No. 434 of 2021], dismissed the Revenue’s appeal and confirmed that CERs earned under the CDM mechanism in wind energy operations were a capital receipt, not taxable as business income. The Court relied on the Karnataka and Andhra Pradesh precedents and on S.P. Spinning Mills Pvt. Ltd. v. ACIT [2021 (1) TMI 1081 (Madras HC)] [5]. Multiple ITAT benches — at Jaipur in Shree Cement Ltd. v. ACIT [(31 ITR (Trib.) 513)], at Chennai in Ambica Cotton Mills Ltd. v. Dy. CIT [(27 ITR (Trib.) 44)], and at Ahmedabad in 2023 — consistently followed the same line [6].

Section 115BBG: The Legislative Intervention of 2017

To bring an end to years of protracted litigation, the Finance Act, 2017 inserted Section 115BBG into the IT Act, operative from 1 April 2018 (Assessment Year 2018-19 onwards). The stated objective was “to bring clarity on the issue of taxation of income from transfer of carbon credits and to encourage measures to protect the environment” [1].

The text of Section 115BBG reads as follows:

“115BBG. (1) Where the total income of an assessee includes any income by way of transfer of carbon credits, the income-tax payable shall be the aggregate of — (a) the amount of income-tax calculated on the income by way of transfer of carbon credits, at the rate of ten per cent; and (b) the amount of income-tax with which the assessee would have been chargeable had his total income been reduced by the amount of income referred to in clause (a). (2) Notwithstanding anything contained in this Act, no deduction in respect of any expenditure or allowance shall be allowed to the assessee under any provision of this Act in computing his income referred to in clause (a) of sub-section (1). Explanation — For the purposes of this section, ‘carbon credit’ in respect of one unit shall mean a reduction of one tonne of carbon dioxide emissions or emissions of its equivalent gases which is validated by the United Nations Framework on Climate Change and which can be traded in the market at its prevailing market price.” [7]

On a careful reading, Section 115BBG does not categorise carbon credit proceeds as either a capital receipt or a revenue receipt — it merely taxes “income by way of transfer of carbon credits.” There is no corresponding amendment to Section 2(24) or Section 28, meaning legal practitioners have argued that the existing case law holding CERs to be capital receipts remains relevant. The 10% rate operates on the gross amount with no deductions permitted — which imposes a higher effective burden than a normal profits-based tax. The section applies to both resident and non-resident assessees, though for non-residents, taxability arises only to the extent attributable to a business connection or permanent establishment in India [1].

The Voluntary Carbon Credit Problem and Satia Industries

A significant ambiguity stems from the narrow definition in the Explanation to Section 115BBG, which restricts “carbon credit” to reductions “validated by the United Nations Framework on Climate Change.” Voluntary carbon credits — validated by independent bodies such as Verra (formerly Verified Carbon Standard) or Gold Standard — are arguably outside Section 115BBG entirely. The ITAT, Amritsar, in Satia Industries Ltd. v. NFAC, held precisely this: Renewable Energy Certificates (RECs), regulated by the Central Electricity Regulatory Commission and not by the UNFCCC, are not “carbon credits” within the meaning of Section 115BBG, and proceeds from their transfer remain capital receipts exempt from tax [2]. This creates a notable divergence — entities trading UNFCCC-validated CERs face a 10% gross tax, while entities dealing in voluntary or REC markets may claim full capital receipt exemption.

The Regulatory Framework: Energy Conservation (Amendment) Act, 2022 and the CCTS

India’s engagement with carbon credits began under the Kyoto Protocol’s CDM. The institutional foundation for a domestic carbon trading market, however, took decades to develop. The Energy Conservation (Amendment) Act, 2022 — which amended the Energy Conservation Act, 2001 — provided the first statutory basis for a domestic Carbon Credit Trading Scheme (CCTS). Section 14(w) of the Energy Conservation Act (as amended) empowers the Central Government to “specify the carbon credit trading scheme,” while Section 2(da) allows the Central Government or any authorised agency to issue Carbon Credit Certificates (CCCs), with each CCC representing one tonne of CO2-equivalent reduction [8].

The Ministry of Power formally notified the CCTS in June 2023, establishing the Indian Carbon Market (ICM). The ICM has a two-tier structure — a compliance mechanism targeting energy-intensive sectors with mandatory GHG emission intensity targets, and a voluntary offset mechanism open to non-obligated entities. The Bureau of Energy Efficiency (BEE) acts as market administrator; the Grid Controller of India (GCI) serves as the central registry; and the Central Electricity Regulatory Commission (CERC) regulates trading through approved power exchanges [9]. On 8 October 2025, the Ministry of Environment, Forest and Climate Change notified the Greenhouse Gas Emission Intensity Target Rules, 2025, covering 282 entities across aluminium, cement, chlor-alkali and pulp and paper sectors — marking the transition from policy framework to operational compliance for India’s nascent carbon market.

Conclusion and Classification

The income tax treatment of carbon credits in India has moved through identifiable phases. For assessment years prior to 2018-19, courts have consistently held CERs to be capital receipts outside the scope of any head of income, and accordingly not liable to tax. For AY 2018-19 onwards, Section 115BBG imposes a 10% flat rate on gross income from UNFCCC-validated carbon credit transfers, with no deductions allowed. Voluntary credits outside the UNFCCC framework fall back into capital receipt territory under the pre-amendment case law. Carbon credits are best characterised as a sui generis instrument — neither a capital asset under Section 2(14) (because capital gains computation fails) nor a revenue receipt in the traditional sense (because they arise from environmental entitlement, not business output). Section 115BBG has carved out a special legislative category without resolving the underlying conceptual debate. The Supreme Court’s eventual ruling in Lanco Tanjore will be definitive.

References

[1] Sachin Kumar B P and Akella A.S. Prakasa Rao, “Conundrum of Taxing Carbon Credits in India,” Tax Sutra Expert Articles, available at: https://database.taxsutra.com/articles/247e49018231c072087302cf158168/expert_article

[2] AZB & Partners, “Sale of Renewable Energy Certificates Not Covered Under Section 115BBG,” AZB Legal Update, July 2023, available at: https://www.azbpartners.com/bank/sale-of-renewable-energy-certificates-not-covered-under-section-115bbg-oust-taxability-by-holding-it-a-capital-receipt/

[3] My Home Power Ltd. v. DCIT, ITA No. 1114/Hyd/2009, ITAT Hyderabad, 02.11.2012 (affirmed by A.P. High Court, ITAT Appeal No. 60 of 2014, 19.02.2014), available at: https://indiankanoon.org/doc/146055938/

[4] “Taxability of Carbon Credits,” BCA Journal Online, November 2023, available at: https://bcajonline.org/journal/taxability-of-carbon-credits/

[5] “Sale of Carbon Credits is Capital Receipt and Not Taxable” (CIT v. Wescare (India) Ltd., Madras HC, Tax Case Appeal No. 434 of 2021), Tax Guru, September 2021, available at: https://taxguru.in/income-tax/sale-carbon-credits-capital-receipt-taxable.html

[6] “Profit from Sale of Carbon Credit is Capital Receipt, Not Taxable: ITAT,” Tax Scan, January 2023, available at: https://www.taxscan.in/profit-from-sale-of-carbon-credit-is-capital-receipt-not-taxable-itat-read-order/249810/

[7] “Taxability of Carbon Credits — Full Text of Section 115BBG,” Tax Guru, December 2019, available at: https://taxguru.in/income-tax/taxability-carbon-credits.html

[8] PRS India, “The Energy Conservation (Amendment) Bill, 2022,” PRS Legislative Research, available at: https://prsindia.org/billtrack/the-energy-conservation-amendment-bill-2022

[9] Bureau of Energy Efficiency, Ministry of Power, “National Carbon Market Framework,” Government of India, available at: https://www.beeindia.gov.in/carbon-market.php