Whatsapp

Whatsapp

Livestream Donations and the TDS Gap on Creator Income in India: Why Streamers and Influencers Have No Withholding

Introduction India’s creator economy has grown into a multi-billion-rupee ecosystem, where gaming streamers attract thousands of viewers, YouTubers monetize every upload, and

Startup Losses and Section 79 of the Income Tax Act, 1961: When Anti-Abuse Rules Kill Legitimate Restructuring

Introduction India’s startup ecosystem has grown into one of the most dynamic in the world, yet founders and investors continue to grapple with a tax provision that was never

Fractional Ownership of Real Estate and Income Tax: How Co-Ownership Platforms Fall Through the Cracks of Section 54 and 54F

Introduction Fractional ownership of real estate has moved from a niche arrangement between family members and business partners to a fully commercialised, technology-enabled inves

Section 56(2)(viib) Angel Tax Abolition 2024: Retrospective Refund Rights of Startups Assessed Between 2012–2024

The Twelve-Year Burden: What Was Angel Tax? When Finance Minister Pranab Mukherjee introduced the Finance Act, 2012, he inserted a clause into the Income Tax Act, 1961 that would g

Comprehensive Treatise on Capital Gains Tax on the Sale of Agricultural Land in India

Chapter 1: Constitutional and Statutory Genesis of Agricultural Taxation The taxation of agricultural land in India is not merely a matter of fiscal statute but a subject deeply ro

Non-Compete Fee Can Be Deducted As Revenue Expenditure Under Section 37(1) Income Tax Act: Supreme Court Clarifies Long-Standing Controversy

Introduction The Indian Supreme Court has recently delivered a landmark judgment that has far-reaching implications for corporate taxation in the country. In Sharp Business System

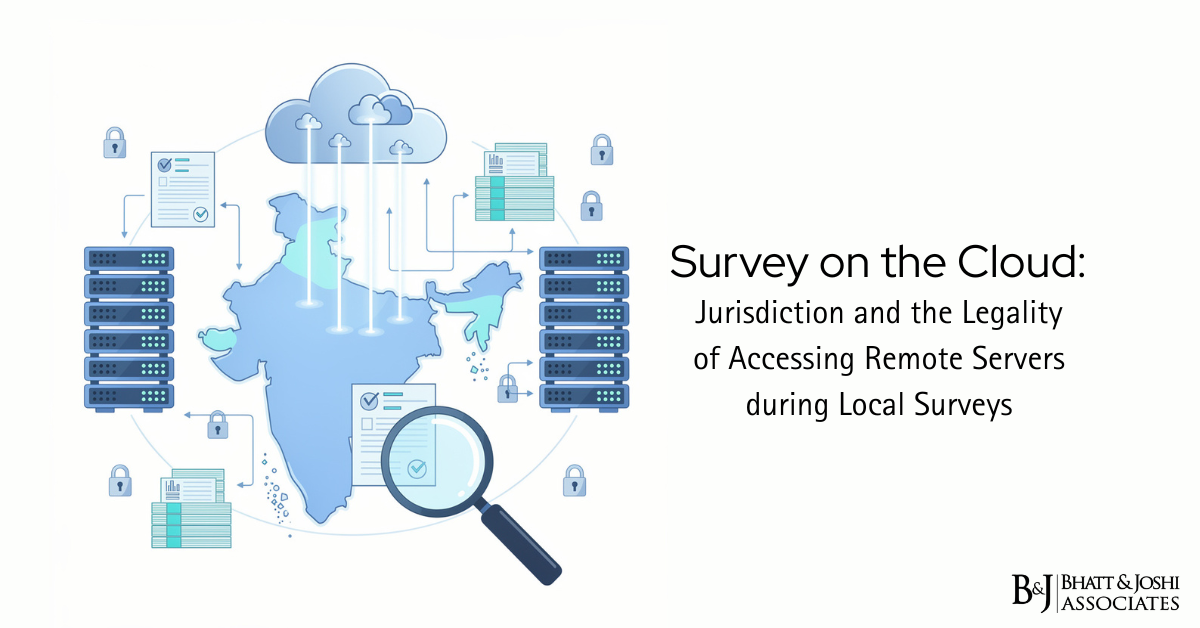

Cloud Data Access During Income Tax Surveys in India: Legal Framework & Jurisdictional Challenges”

Introduction The digital transformation has fundamentally altered regulatory compliance and enforcement mechanisms in India. As organizations migrate to cloud-based infrastructure,

CBDT Office Memorandum 2025: Risk Management Strategy (RMS) Exemption for Search and Survey Cases – Streamlining Reassessment or Legal Loophole?

Introduction The Central Board of Direct Taxes (CBDT) issued an Office Memorandum on February 27, 2025, fundamentally altering how search and survey case information flows through

Survey Authorization for Entity A, Documents Found for Entity B: Section 153C Third-Party Tax Assessment, Section 292C Presumption Trap, and Group Company Liability

Understanding the Jurisdictional Anomaly in Tax Assessments During tax enforcement proceedings, the Income Tax Department often encounters a peculiar situation where survey or sear

Section 14A/Mat Disallowances: Section 14A Disallowance: A Comprehensive Assessee Defense Strategy Across DRP, CIT(A), and ITAT

1. INTRODUCTION: THE ASSESSEE’S STRATEGIC LANDSCAPE Understanding the Asymmetry The relationship between the tax department and the assessee is inherently asymmetrical. The D