Whatsapp

Whatsapp

E-Invoicing Threshold Limit of Rs. 5 Crore: Analyzing the Digital Divide Between Tier-1 and Tier-3 Businesses

Introduction

India’s Goods and Services Tax regime has always carried within it an ambitious undertaking — not just fiscal reform, but the wholesale digitalisation of how business is transacted across a country of staggering geographic and economic diversity. When the Central Board of Indirect Taxes and Customs (CBIC) issued Notification No. 10/2023 – Central Tax dated 10th May 2023, it did far more than reduce a threshold. It pulled approximately four lakh additional businesses [1] into the ambit of electronic invoicing, effective 1st August 2023 — entities that, by their very nature and location, are often the least equipped to absorb such compliance demands overnight.

The mandate is clear enough in its legal text. In the said notification, amending the principal Notification No. 13/2020 – Central Tax dated 21st March 2020, the government reduced the threshold for mandatory e-invoicing to Rs. 5 crore, effectively setting the E-Invoicing Threshold Limit. This change made e-invoicing compulsory for every GST-registered business whose Annual Aggregate Turnover (AATO) exceeded Rs. 5 crore in any financial year from 2017-18 onwards. What followed, however, exposed a fault line that tax policy in India has long struggled to address — the yawning digital divide between businesses in Tier-1 metropolitan centres and those operating out of Tier-2 and Tier-3 cities, small towns, and semi-urban pockets across the country.

This article examines the regulatory architecture that governs e-invoicing, the phased rollout that led to the current threshold limit, the structural asymmetry in technological readiness between different business tiers, and the legal consequences that follow non-compliance — including judicial interpretations that have shaped how penalty provisions operate.

The Legal Framework: From Notification to Non-Negotiable Compliance

The authority for e-invoicing derives from sub-rule (4) of Rule 48 of the Central Goods and Services Tax Rules, 2017, which empowers the government to notify a class of registered persons who must prepare invoices by uploading specified particulars in Form GST INV-01 to the Invoice Registration Portal (IRP) and obtain an Invoice Reference Number (IRN) [2]. Sub-rule (5) of the same Rule completes the enforcement architecture — an invoice issued in any other manner by a notified person shall not be treated as a valid invoice for the purposes of the CGST Act. This is not a procedural irregularity that can be cured after the fact. It strikes at the root of Input Tax Credit (ITC) eligibility.

This dual mechanism — mandatory registration of invoices through the IRP, coupled with the invalidation of any non-compliant invoice — effectively makes the e-invoice system self-reinforcing. Buyers in a supply chain who receive invoices that lack a valid IRN and QR code risk being denied ITC, creating commercial pressure across the chain for upstream compliance. The IRP, upon receiving invoice data in the prescribed JSON format, validates it, digitally signs it, and generates the IRN along with a QR code, which must then appear on every invoice issued to a registered buyer [2].

Notification No. 13/2020 – Central Tax, published in the Gazette of India on 21st March 2020, originally introduced this framework for businesses with AATO exceeding Rs. 500 crore [3]. The phased rollout thereafter was methodical: Rs. 100 crore (January 2021), Rs. 50 crore (April 2021), Rs. 20 crore (April 2022), Rs. 10 crore (October 2022), and finally Rs. 5 crore effective August 2023 [3]. Each phase, in theory, was designed to give the next tranche of businesses time to prepare — to upgrade billing software, integrate with GST Suvidha Providers (GSPs), test in the GSTN sandbox environment, and train their personnel. In practice, the adequacy of that preparation time has varied dramatically depending on where in the country a business is located and what technological infrastructure it has access to.

The Exempted Categories: Who Is Spared

Not every business above the Rs. 5 crore threshold limit falls within the e-invoicing mandate. Rule 48(4) of the CGST Rules, read together with the notifications issued thereunder, exempts certain categories of entities altogether — regardless of their turnover. These include insurers, banking companies, financial institutions (including Non-Banking Financial Companies or NBFCs), Goods Transport Agencies (GTAs), suppliers of services such as cinema exhibition in multiplex screens, Special Economic Zone (SEZ) units (exempted via CBIC Notification No. 61/2020 – Central Tax), government departments and local authorities (exempted via CBIC Notification No. 23/2021 – Central Tax), and persons registered as Online Information Database Access and Retrieval (OIDAR) service providers under Rule 14 of the CGST Rules.

The rationale for these carve-outs is largely structural. Regulated financial entities already operate within well-supervised digital reporting ecosystems. SEZ units operate under a distinct statutory regime under the Special Economic Zones Act, 2005. Transport agencies and cinema service providers have sector-specific compliance frameworks. What is striking, however, is that the businesses which fall most squarely within the mandate — the wholesale traders, manufacturers, and service providers in the Rs. 5–10 crore bracket — are precisely those who have the thinnest technology budgets, the least access to skilled compliance staff, and the greatest exposure to connectivity challenges.

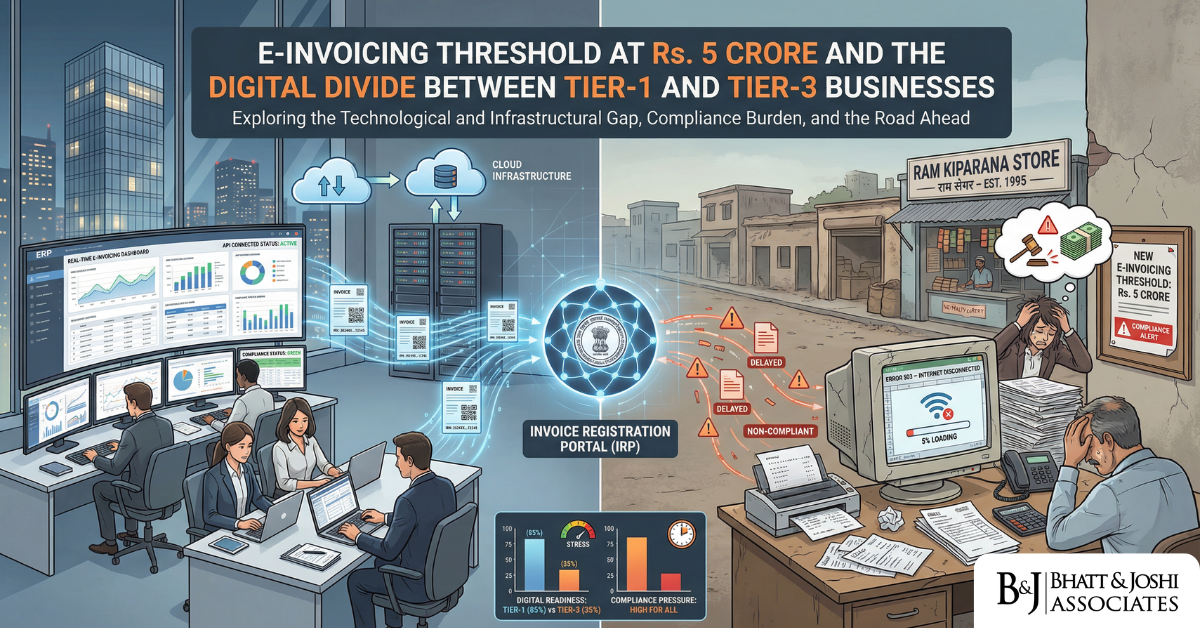

Tier-1 vs. Tier-3 Businesses: Where the Divide Runs Deepest

A large enterprise headquartered in Mumbai, Bengaluru, or Delhi typically operates enterprise resource planning (ERP) software that can be configured to push invoice data directly to the IRP via an Application Programming Interface (API), either through a GSP or through the GSTN’s direct integration. The invoice generation, IRN capture, QR code embedding, and auto-population of GSTR-1 are, for such businesses, a matter of system integration that their IT teams or outsourced technology vendors handle largely in the background [1].

The picture is categorically different for a textile trader in Bhilwara, a hardware supplier in Ludhiana’s smaller wholesale markets, a chemical distributor in Ankleshwar, or a food processor in a Tier-3 town in Bihar. These businesses may operate on basic billing software that was never designed with API connectivity in mind. Their internet connectivity is intermittent at best — a reality that directly undermines the real-time nature of IRN generation, which must occur before or at the point of issuing each invoice [1]. When the GSTN’s servers themselves have experienced downtime, larger businesses absorb the disruption with internal buffer processes; smaller ones face transaction paralysis.

The technological challenge is compounded by the human capital gap. Compliance with e-invoicing requires not just software, but an understanding of JSON data formats, HSN code accuracy, GSTIN validation of buyers, and the technical error codes generated when the IRP rejects an invoice upload. Businesses in metro cities typically have dedicated accounts teams or outsource to specialist CA firms that are well-versed in GST technology. A Rs. 6 crore turnover enterprise in a Tier-3 district may have a single accountant who manages everything from inventory to returns, and whose familiarity with digital compliance is limited to the basics of GSTR-3B filing [4].

Over 73% of MSMEs in semi-urban and rural India have reported business growth after adopting digital tools, but the transition itself has not been painless [4]. The compliance pressure introduced by e-invoicing is not a simple extension of existing processes — it is a structural transformation of how every B2B transaction is documented. For businesses that still deal heavily in handwritten vouchers or basic Tally entries reconciled at the end of the month, the demand for real-time invoice reporting represents a fundamental shift in their operating model.

Penalties for Non-Compliance and the Judicial Response

The consequences of failing to comply with the e-invoicing mandate are not trivial. Section 122(1) of the Central Goods and Services Tax Act, 2017 provides for a penalty of Rs. 10,000 or an amount equivalent to the tax evaded or ITC wrongly availed or passed on, whichever is higher, for a range of specified offences — including supplying goods or services without issuing a valid invoice [3]. Since an invoice without an IRN is not a “valid invoice” under Rule 48(5) of the CGST Rules, every non-compliant B2B invoice technically constitutes an offence under this provision.

The text of the relevant provision is instructive. Section 122(1) reads, in relevant part, that a taxable person who “supplies any goods or services or both without issue of any invoice or issues an incorrect or false invoice with regard to any such supply” shall be liable to pay a penalty of “ten thousand rupees or an amount equivalent to the tax evaded… or the input tax credit availed of or passed on or distributed irregularly, or the refund claimed fraudulently, whichever is higher.” For a business issuing hundreds of B2B invoices per month without IRN, the cumulative exposure under this section is severe [3].

The Allahabad High Court’s decision in M/s Metenere Ltd. v. Union of India and Another [Writ Tax No. 360 of 2020, dated 17th December 2020] is an important reference point for how courts have approached the proportionality of GST penalties. The Court, while dealing with a dispute over non-maintenance of records and alleged duty evasion, held that offences under Section 122 of the CGST Act must be distinguished — those involving an intention to evade tax attract the higher penalty tied to the tax amount, whereas procedural violations without evidence of evasion attract only the minimum Rs. 10,000 penalty [5]. The Court reduced a penalty of Rs. 19,43,89,804 to Rs. 10,000 because no exercise for quantification of evaded tax had been conducted and the violation related to non-maintenance of records, not actual evasion. This principle carries significant implications for how tax authorities should treat technical non-compliance with e-invoicing rules by small businesses that are not engaged in fraudulent invoicing.

Separately, the broader enforcement framework for invoice fraud has been tightened. Section 122(1A) of the CGST Act, inserted effective 1st January 2021, imposes penalties on any person — whether or not a registered taxable person — who retains the benefit of transactions involving supply without invoice, invoice without supply, wrongful ITC availment, or fraudulent refunds, and at whose instance such transactions are conducted [6]. This provision was designed to catch the principals behind fake invoice networks. The Supreme Court, in a matter involving Mukesh Kumar Garg [SLP arising from Delhi High Court judgment in W.P.(C) 9141/2025], has stayed recovery and agreed to examine substantial questions of law regarding the retrospective application of Section 122(1A) — a question that has significant implications for how the provision is deployed against those alleged to have operated ghost firms to avail fictitious ITC [6].

The practical consequence for buyers in a supply chain is equally serious. Where a supplier fails to generate a valid e-invoice and the buyer accepts such an invoice and claims ITC on it, the buyer risks an ITC reversal. Rule 48(5) makes the invoice itself invalid, and without a valid tax invoice, the conditions for ITC eligibility under Section 16(2) of the CGST Act, 2017 — which requires possession of a tax invoice issued by the supplier — are not met. The downstream financial impact falls on parties who may have had no knowledge of the upstream compliance failure.

The Structural and Policy Problem With a Uniform Threshold

The Rs. 5 crore e-invoicing threshold limit under GST applies uniformly across all registered entities in every sector and geography, subject only to the category-based exemptions described above. It draws no distinction between a manufacturer in an industrial estate near Chennai with robust ERP systems and an FMCG distributor in a small town in Jharkhand who processes most transactions through basic software. This one-size-fits-all approach has attracted criticism from trade associations and practitioners, who have argued that the government should consider geographic or sectoral calibration of the compliance timeline, at least for the initial period of each phase. [4].

From the ITC chain perspective, the pressure is even more acute. When a large buyer with Rs. 500 crore turnover transacts with a newly onboarded supplier at the Rs. 5–10 crore level, the buyer’s ITC reconciliation system immediately flags invoices without IRNs. The buyer’s accounts payable team withholds payment or demands rectification, placing commercial pressure on the small supplier that the GST law, by itself, does not impose. This informal market enforcement mechanism accelerates compliance among suppliers who can adapt, but creates significant working capital stress for those who cannot [4]. The net effect is that the compliance burden concentrates at the weaker end of the supply chain — not because larger firms are more virtuous, but because they have the negotiating power to enforce upstream compliance that protects their own ITC.

Connectivity is not merely an urban-rural binary. Many small manufacturing towns — the Tiruppur knitwear clusters, the Moradabad brassware markets, the Rajkot engineering hubs — operate with moderate internet access but lag significantly in digital financial literacy. The GSTN has enabled a sandbox environment for testing since July 2022, which in theory allows businesses to validate their e-invoicing integration before going live [1]. But accessing and using the sandbox meaningfully requires a level of technical capacity that many businesses in this bracket simply do not have in-house, and the cost of engaging a GSP or technical consultant adds to what is already a margin-thin operating environment.

The Way Forward: Compliance Support and Future Threshold Reductions

Industry discussion has increasingly pointed to the likelihood of a further reduction in the e-invoicing threshold limit — potentially to Rs. 2 crore — which would pull an even larger number of small and micro businesses into the compliance net [4]. If that step is taken without addressing the underlying infrastructure deficit, the problems that have characterised the current phase will be replicated at greater scale and intensity.

What is needed is not simply a notification amending a threshold but a parallel programme of compliance support: government-facilitated access to affordable e-invoicing solutions for small businesses, concentrated connectivity infrastructure upgrades in Tier-2 and Tier-3 regions, and publicly funded digital literacy campaigns targeted specifically at business owners rather than accountants. The GSTN’s offline tools and API integration options offer a menu of technical solutions, but they assume a minimum baseline of digital capability that is still absent in a significant portion of businesses in this turnover bracket.

India’s e-invoicing ambition is structurally sound. The objective — reducing ITC fraud, creating a real-time audit trail, eliminating fake invoicing, and auto-populating GST returns — is both legitimate and important for the long-term integrity of the tax system. The legal machinery through which it operates, from Rule 48(4) of the CGST Rules to the penalty architecture of Section 122 of the CGST Act, is robust. What has lagged behind is the honest reckoning with the fact that imposing uniform compliance obligations across a country as economically diverse as India, without proportionate investment in closing the digital divide, shifts the burden most heavily onto those least able to bear it.

Conclusion

The reduction of the e-invoicing threshold limit to Rs. 5 crore under Notification No. 10/2023 – Central Tax was a necessary step in expanding India’s digital tax infrastructure. It is legally well-grounded in Rule 48(4) of the CGST Rules and forms part of a carefully phased rollout that began at the Rs. 500 crore level in October 2020. But legal correctness and practical equity are not the same thing. For Tier-1 businesses with established technology stacks and compliance teams, this was an integration exercise. For a significant number of businesses in Tier-3 cities and semi-urban India, it represented a compliance transformation that their current infrastructure was not designed for.

The judicial guidance, particularly from the Allahabad High Court’s decision in M/s Metenere Ltd., provides some basis for proportionate enforcement — distinguishing between procedural failures and deliberate evasion. But proportionate enforcement after the fact is no substitute for proportionate policy design before the fact. As the government considers the next phase of threshold reduction, the digital divide must be addressed as a precondition, not an afterthought.

References

[1] ClearTax, E-Invoice Limit 5 Crore: E-Invoicing Mandatory for Businesses Above Rs. 5 Crore Turnover (last updated December 16, 2024). Available at: https://cleartax.in/s/e-invoicing-businesses-above-rs-5-crore-turnover

[2] IRIS IRP (GSTN Certified IRP), E-Invoice under GST as per Rule 48(4) of CGST Rules 2017. Available at: https://einvoice6.gst.gov.in/content/e-invoice-under-gst-as-per-rule-484-of-cgst-rules-2017/

[3] TaxGuru, GST E-Invoicing Limit Reduced to Rs. 5 Crore from 01st August 2023 (May 15, 2023). Available at: https://taxguru.in/goods-and-service-tax/gst-e-invoicing-limit-reduced-rs5-crore-01st-august-2023.html

[4] Binary Semantics, GST Compliance for SMEs in India: Challenges & Tech (2025). Available at: https://www.binarysemantics.com/blogs/start-ups-and-smes-gst-compliance-in-india-growing-pains-tech-levers-the-future-ahead/

[5] Indian Kanoon, M/S Metenere Ltd. v. Union of India and Another [Writ Tax No. 360 of 2020, Allahabad High Court, December 17, 2020]. Available at: https://indiankanoon.org/doc/70402221/

[6] A2Z Taxcorp LLP, Supreme Court Stays Retrospective GST Penalty under Section 122(1A) and to Examine its Applicability to Non-Taxable Persons (September 2025). Available at: https://a2ztaxcorp.net/supreme-court-stays-retrospective-gst-penalty-under-section-1221a-and-to-examine-its-applicability-to-non-taxable-persons/

[7] Press Information Bureau (PIB), GST Taxpayers Get Relief in Implementation of E-Invoice (October 2020). Available at: https://www.pib.gov.in/Pressreleaseshare.aspx?PRID=1660533

[8] IndiaFilings, Mandatory GST E-Invoicing for Taxpayers Exceeding Threshold Limit of INR 5 Crore. Available at: https://www.indiafilings.com/learn/mandatory-gst-e-invoicing-for-taxpayers-exceeds-threshold-limit-of-inr-5-crore/

[9] CBIC Official Tax Information Portal, Section 122 of the Central Goods and Services Tax Act, 2017. Available at: https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_CGST_act/active/chapter19/section122_v1.00.html