Whatsapp

Whatsapp

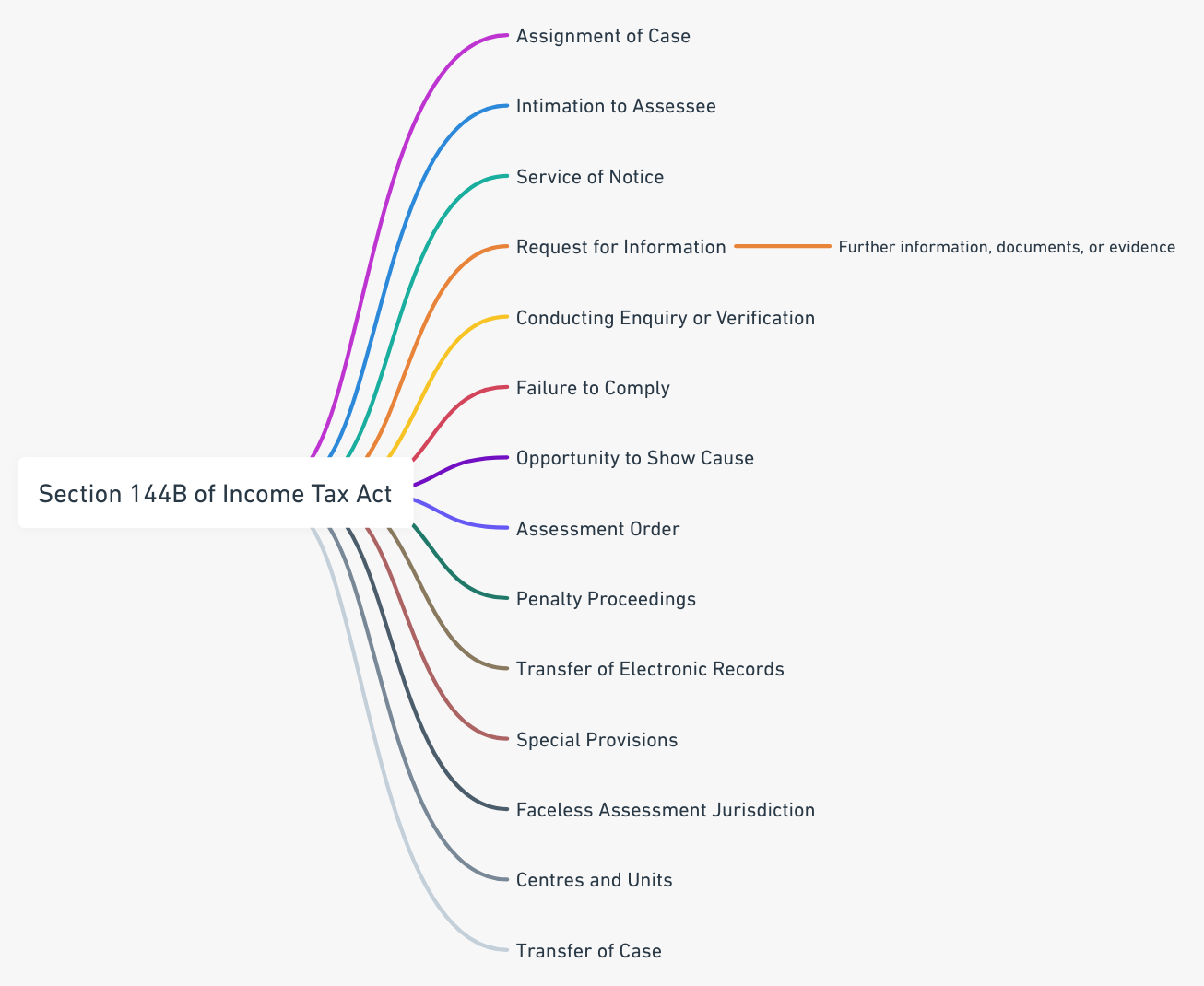

Faceless Assessment Procedure under Section 144B of Income Tax Act- Part 4

Introduction

Until now, we have discussed the Introduction of Faceless Assessment, assignment of cases and communication of response in Part 1, & request for information and documents, conducting enquiry or verification, failure to comply, opportunity to show cause, filing of response in Part 2. Now, we shall discuss provisions related to draft and final assessment orders, penalty proceedings and transfer of electronic records. Now, we shall discuss provisions related to draft and final assessment orders, penalty proceedings, and the transfer of electronic records. Building on this, the transformation of India’s tax administration through digital innovation reached a significant milestone with the introduction of the faceless assessment regime under Section 144B of the Income Tax Act, 1961. Designed to eliminate physical interface between taxpayers and assessing officers, this revolutionary mechanism promotes transparency, accountability, and efficiency in the assessment process.

Operated through the National Faceless Assessment Centre (NaFAC), the system coordinates with specialized units to ensure that tax assessments are conducted in an unbiased, technology-driven manner [1]. While the basic framework has streamlined routine tax evaluations, the legislation also recognizes that certain cases require special attention due to their inherent complexity. Section 144B incorporates provisions addressing complex assessments, territorial jurisdiction, and case transfers when circumstances demand a more traditional approach. These measures ensure that the faceless system remains flexible enough to handle extraordinary situations while maintaining its core principles.

Understanding these provisions is critical for tax practitioners, assessees, and revenue authorities alike, as they represent sophisticated legal mechanisms that balance technological advancement with practical considerations of tax administration. This article examines these advanced aspects of the faceless assessment procedure, exploring their function within the broader statutory framework and implications for tax compliance and administration.

Special Provisions for Complex Cases

The Income Tax Act acknowledges that not all assessment cases are identical in their complexity or requirements. Certain assessments involve intricate financial transactions, voluminous documentation, specialized business activities, or accounts whose accuracy may be questionable. For such situations, Section 144B provides special provisions that allow the assessment machinery to adopt a more intensive scrutiny process while remaining within the faceless assessment framework [2].

When the assessment unit examines a case and identifies factors that suggest heightened complexity, it possesses the authority to invoke special provisions designed specifically for such circumstances. The determination of complexity is not arbitrary but must be based on objective criteria established within the statutory framework. These criteria include the nature and complexity of the accounts being examined, the volume of financial records and transactions involved, legitimate doubts regarding the correctness or completeness of the accounts, the multiplicity of transactions which may indicate complex business operations, and the specialized nature of the business activity undertaken by the assessee.

The assessment unit’s decision to classify a case as complex must be grounded in a careful evaluation of these factors, with due consideration given to the interests of revenue. This means that the potential impact on government revenues forms an important consideration when determining whether special provisions should be applied. The legislative intent behind these provisions is to ensure that cases requiring deeper investigation receive appropriate attention without compromising the faceless nature of the assessment process.

Once the assessment unit determines that a case falls within the category requiring special provisions, it must formally refer the matter to the National Faceless Assessment Centre with specific recommendations. This referral triggers a distinct procedural pathway that differs from standard faceless assessments. The most significant aspect of this pathway is the potential invocation of Section 142(2A) of the Income Tax Act, which deals with special audit provisions.

Section 142(2A) empowers the assessing authority to direct that the accounts of an assessee be audited by an accountant nominated by the Principal Chief Commissioner or Principal Director General of Income Tax [3]. This special audit provision serves as a powerful tool for examining complex financial arrangements and business transactions that may not be adequately addressed through regular assessment procedures. The nominated accountant must be a qualified chartered accountant who is not already associated with the assessee’s routine audit work, thereby ensuring independence and objectivity in the examination process.

The special audit conducted under Section 142(2A) goes beyond the scope of regular statutory audits mandated under Section 44AB of the Income Tax Act. While statutory audits focus on general compliance and financial statement verification, special audits are directed toward specific aspects of the assessee’s accounts that have raised concerns during the assessment process. The chartered accountant conducting the special audit must furnish a detailed report addressing the specific issues identified by the assessment unit, and this report becomes a crucial piece of evidence in the assessment proceedings.

The procedural safeguards built into the special audit mechanism ensure that it is not employed arbitrarily. Before directing a special audit, the assessing authority must form a bona fide opinion that such audit is necessary considering the complexity and nature of the accounts, and this opinion must be documented in writing. The assessee must be given an opportunity to be heard before the special audit is ordered, as mandated by principles of natural justice that permeate tax administration procedures.

It is important to note that the invocation of special provisions does not necessarily remove the case from the faceless assessment framework entirely. Rather, it allows for specialized technical input and deeper scrutiny while maintaining the essential character of faceless proceedings. The assessment unit continues to handle the case through electronic means, incorporating the findings of the special audit into the overall assessment process. This hybrid approach leverages the benefits of both technological efficiency and specialized human expertise where circumstances warrant such intervention.

The costs associated with special audits are also addressed within the statutory framework. The expenses of the audit, subject to limits prescribed by the Central Board of Direct Taxes, are borne by the Central Government. This ensures that the financial burden of compliance with special audit requirements does not fall disproportionately on assessees, even though the audit itself is necessitated by concerns about their financial reporting. The prescribed limits on audit fees ensure that expenses remain reasonable and proportionate to the complexity of the case.

Jurisdictional Framework for Faceless Assessment

The concept of territorial jurisdiction has been fundamental to Indian tax administration since its inception. Traditionally, assessing officers operated within defined geographical boundaries, with each officer having jurisdiction over assessees located within a specific territorial area. The faceless assessment regime represents a paradigm shift from this traditional model, introducing a system where physical location becomes less relevant to the assessment process [4].

Section 144B specifically addresses jurisdictional issues by empowering the Central Board of Direct Taxes to determine the scope and coverage of faceless assessment proceedings. The Board possesses broad discretionary authority to specify the territorial areas, persons, classes of persons, incomes, classes of incomes, cases, or classes of cases that will be subject to faceless assessment. This flexible jurisdictional framework allows the tax administration to gradually expand the scope of faceless assessments based on operational readiness and systemic capacity.

The jurisdictional provisions serve multiple purposes within the faceless assessment architecture. First, they enable a phased implementation approach, allowing the tax department to refine procedures and address technical challenges before expanding coverage. When the faceless assessment system was initially rolled out, it applied to a limited subset of cases, with gradual expansion as the infrastructure and processes matured. This measured approach helped minimize disruption to tax administration while allowing for course corrections based on practical experience.

Second, the jurisdictional specifications allow the Board to exclude certain categories of cases that may not be suitable for faceless processing due to their unique characteristics. For instance, cases involving issues of international taxation, cases requiring extensive physical verification of assets, or cases with significant hearing requirements might be excluded from faceless assessment if deemed necessary. The statutory language provides sufficient flexibility to accommodate such exclusions while preserving the broad application of faceless procedures to the majority of assessments.

The establishment of the National Faceless Assessment Centre represents the institutional manifestation of this jurisdictional framework. The NaFAC serves as the central coordinating authority for faceless assessment proceedings, operating in a centralized manner to ensure consistency and efficiency across the country. Regional Faceless Assessment Centres may be established to support the NaFAC, but they operate as extensions of the centralized system rather than as independent territorial jurisdictions in the traditional sense.

This centralized approach offers several advantages over the traditional territorial jurisdiction model. It facilitates economies of scale by consolidating assessment activities and enabling specialization among assessment personnel. Officers can develop expertise in specific types of business activities or tax issues rather than handling the full range of cases that might arise within a geographical territory. The centralized system also promotes uniformity in the application of tax laws and assessment practices, reducing regional variations that may have existed under the territorial jurisdiction model.

From the assessee’s perspective, the jurisdictional framework under Section 144B means that their case may be handled by assessment units located anywhere in the country, rather than being confined to officers in their local area. All communications occur through electronic means via the designated e-filing portal, eliminating the need for physical presence at any particular office location. This geographic independence can be advantageous for assessees, particularly those who operate in multiple locations or who may have faced challenges in physically accessing traditional assessment offices.

The jurisdictional provisions also address the question of which authority has jurisdiction over various procedural aspects of faceless assessment. The Principal Chief Commissioner or Principal Director General in charge of the National Faceless Assessment Centre exercises supervisory authority over the assessment process, including decisions about case transfers and invocation of special provisions. This clear delineation of authority prevents jurisdictional conflicts and ensures that the faceless assessment system operates smoothly without disputes about which authority should handle particular issues.

Transfer of Cases from Faceless Assessment

While the faceless assessment system represents the default procedure for most cases, the Income Tax Act recognizes that exceptional circumstances may necessitate transferring a case from the faceless regime to a traditional assessing officer. Section 144B incorporates specific provisions governing such transfers, ensuring that they occur only when genuinely necessary and through a transparent, rule-bound process [5].

The authority to initiate case transfers rests with the assessment unit handling the case under the faceless assessment procedure. However, this authority is not absolute and operates subject to important procedural safeguards. The assessment unit cannot unilaterally decide to transfer a case; rather, it must identify specific circumstances that justify such transfer and follow prescribed procedures before any transfer can occur. This structured approach prevents arbitrary or capricious transfers that could undermine the faceless assessment system’s objectives.

The circumstances that may justify transferring a case from faceless assessment to a traditional assessing officer closely mirror those that trigger special provisions for complex cases. These include situations where the nature and complexity of the accounts are such that they cannot be adequately addressed through faceless procedures, where the volume of accounts and documentation is so substantial that electronic processing becomes impractical, where there are serious doubts about the correctness of the accounts that require in-depth investigation, where the multiplicity of transactions indicates complex business arrangements that demand specialized scrutiny, or where the specialized nature of the business activity requires expertise that cannot be effectively applied through faceless means.

Additionally, the interests of revenue serve as an overarching consideration in transfer decisions. If the assessment unit believes that remaining within the faceless assessment framework might compromise the government’s revenue interests, this factor can support a decision to transfer the case. However, the mere invocation of revenue interests is insufficient; the assessment unit must demonstrate specific concerns based on the case’s particular facts and circumstances.

When the assessment unit determines that transfer may be appropriate, it must record its reasons in writing. This documentation requirement serves multiple purposes. It ensures that the decision is based on thoughtful consideration rather than convenience or arbitrary preferences. It creates an administrative record that can be reviewed by supervisory authorities and, if necessary, by appellate forums. It also demonstrates to the assessee that the transfer decision rests on objective grounds related to the case’s characteristics rather than any prejudicial considerations.

After recording reasons, the assessment unit refers the case to the National Faceless Assessment Centre with a recommendation that the provisions of Section 142(2A) may need to be invoked. This referral triggers a review process at the NaFAC level, where senior authorities examine the assessment unit’s reasoning and determine whether transfer is indeed warranted. The referral to NaFAC serves as a quality control mechanism, ensuring that transfers occur only after appropriate oversight.

The actual transfer decision is made by the Principal Chief Commissioner or Principal Director General in charge of the National Faceless Assessment Centre. This senior authority possesses the discretion to transfer the case to an assessing officer having jurisdiction over the matter at any stage of the assessment proceedings. The flexibility to transfer “at any stage” is significant, as it acknowledges that circumstances requiring traditional assessment procedures may become apparent early in the process or may emerge only after substantial faceless assessment work has occurred.

Critically, any transfer decision requires prior approval from the Central Board of Direct Taxes. This additional layer of oversight reflects the importance of maintaining the integrity of the faceless assessment system and ensuring that transfers are not used as a routine escape mechanism from faceless procedures. The Board’s approval requirement introduces a check on the exercise of transfer authority by field officers, ensuring that only genuinely exceptional cases are removed from the faceless system.

The jurisdictional question of which assessing officer should receive the transferred case is addressed through reference to traditional jurisdictional principles. The case is transferred to “the Assessing Officer having jurisdiction over such case,” meaning the officer who would have had jurisdiction under pre-faceless assessment territorial rules. This approach ensures continuity with established jurisdictional frameworks and prevents disputes about which officer should handle the transferred case.

Once a case is transferred out of the faceless assessment framework, it proceeds according to traditional assessment procedures. The assessing officer receiving the transferred case has all the powers and responsibilities associated with regular assessment proceedings, including the authority to issue notices, conduct inquiries, examine witnesses, and pass assessment orders. The work already completed under faceless assessment procedures remains part of the case record and can be utilized by the assessing officer, avoiding unnecessary duplication of effort.

The transfer provisions embody an important principle of administrative flexibility within the faceless assessment system. While the legislation strongly favors faceless procedures as the default approach, it recognizes that rigid insistence on faceless assessment in all circumstances could compromise the quality and effectiveness of tax administration. By providing a controlled mechanism for transferring exceptionally complex or sensitive cases to traditional procedures, Section 144B strikes a balance between innovation and pragmatism in tax administration.

Regulatory Framework and Administrative Guidelines

The statutory provisions of Section 144B operate within a broader regulatory framework established by the Central Board of Direct Taxes. The CBDT has issued various circulars, notifications, and standard operating procedures that provide detailed guidance on implementing faceless assessment provisions, including those relating to special cases, jurisdiction, and transfers. These administrative guidelines translate the broad statutory language into concrete operational procedures that assessment units and assessees must follow.

The standard operating procedures issued by the CBDT specify the workflow for handling complex cases within the faceless assessment framework. They detail the documentation requirements when invoking special provisions, the format for recording reasons when proposing case transfers, the timelines for various procedural steps, and the responsibilities of different functional units involved in the process. These procedures ensure uniformity in how special provisions are applied across different cases and assessment centers.

The CBDT’s regulatory framework also addresses technological aspects of faceless assessment, including the electronic platforms through which all communications must occur. The e-filing portal maintained by the Income Tax Department serves as the primary interface between assessees and the faceless assessment machinery. All notices, responses, submissions, and orders are exchanged through this portal, creating a complete digital trail of the assessment proceedings. The technical specifications for this portal, security protocols, authentication mechanisms, and document format requirements are established through CBDT guidelines.

Recent amendments to Section 144B have refined the faceless assessment procedure based on experiences since its introduction. The Finance Act, 2023 made significant changes aimed at streamlining processes and addressing practical difficulties encountered during implementation. These amendments modified the procedural requirements for various stages of faceless assessment, clarified the roles of different assessment units, and addressed concerns about natural justice and hearing requirements. Understanding these amendments is essential for appreciating the current state of faceless assessment law.

Conclusion

The special provisions of Section 144B governing complex cases, jurisdictional specifications, and case transfers represent sophisticated legal mechanisms that ensure the faceless assessment system can adapt to varying circumstances while maintaining its core principles. These provisions recognize that tax administration must balance the efficiency and transparency offered by technology-driven faceless procedures with the practical reality that some cases require more intensive scrutiny or specialized approaches.

The framework for handling complex cases through special audit provisions under Section 142(2A) demonstrates legislative wisdom in creating pathways for deeper investigation where needed. Similarly, the flexible jurisdictional framework allows the tax administration to calibrate the scope of faceless assessment based on operational capabilities and case characteristics. The controlled mechanism for transferring cases ensures that exceptional situations can be addressed through traditional procedures without undermining the broader shift toward faceless assessment.

As India’s tax administration continues evolving, these special provisions will play an increasingly important role in ensuring that the faceless assessment system remains robust, fair, and effective across the full spectrum of tax cases. Taxpayers and practitioners must understand these provisions to navigate the assessment process effectively, while tax authorities must apply them judiciously to maintain the system’s integrity and public confidence.

References

[1] IndiaFilings. “Section 144B of Income Tax Act: Faceless Assessment.” Available at: https://www.indiafilings.com/learn/section-144b-of-income-tax-act/

[2] ClearTax. “Faceless Assessment Scheme Under Section 144B of Income Tax Act.” Available at: https://cleartax.in/s/e-assessment-scheme-2019

[3] TaxGuru. “Special Audit – Section 142(2A) – Income Tax Act, 1961.” Available at: https://taxguru.in/income-tax/special-audit-section-1422a-income-tax-act-1961.html

[4] TradeViser. “Section 144B of Income Tax Act: Faceless Assessment Scheme Explained.” Available at: https://tradeviser.in/2025/06/25/section-144b-of-income-tax-act-faceless-assessment-scheme-explained/

[5] TaxGuru. “Faceless assessment not valid if Section 144B procedure not complied.” Available at: https://taxguru.in/income-tax/faceless-assessment-valid-section-144b-procedure-complied.html