Whatsapp

Whatsapp

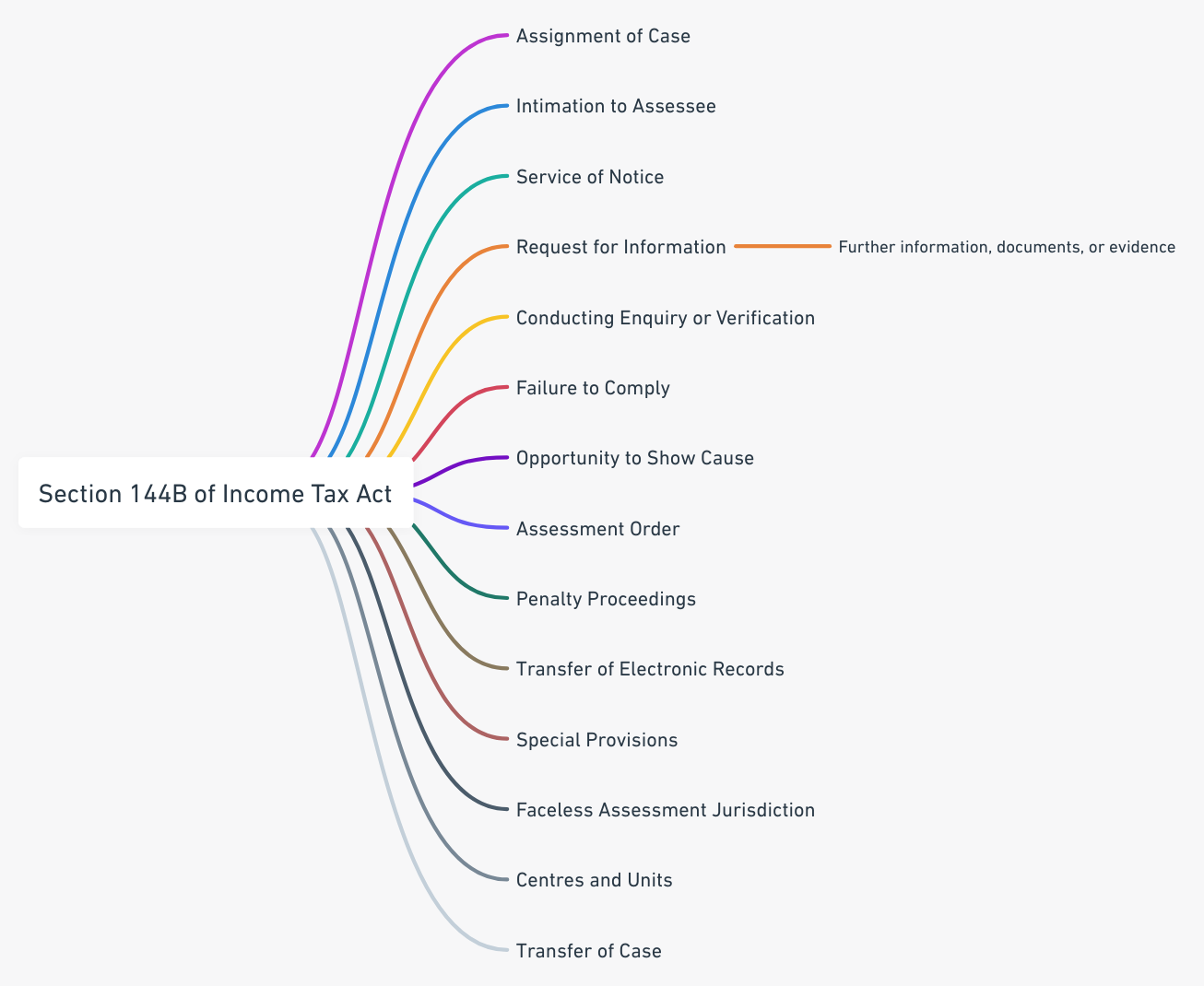

Section 144B Income Tax Act: Show Cause Notice Stage Explained

Introduction

Until now, we have discussed the Introduction of Faceless Assessment, assignment of cases and communication of response in Part 1, & request for information and documents, conducting enquiry or verification, failure to comply, opportunity to show cause, filing of response in Part 2. Now, we shall discuss provisions related to draft and final assessment orders, penalty proceedings and transfer of electronic records.

Assessment Order

The purpose of passing the assessment order under Section 144B is to outline the systematic and transparent procedure for conducting faceless assessments of taxpayers.. This process aims to ensure fair and impartial assessments while providing opportunities for taxpayers to participate and respond to proposed variations in their tax liabilities.

- Preparation of Draft Order: The assessment unit prepares a draft order after considering all relevant material, including the response from the assessee and any review report.

- Service of Draft Order: In case of an eligible assessee where there is a proposal to make any variation prejudicial to the interest of the assessee, the National Faceless Assessment Centre serves the draft order on the assessee.

- Assessee’s Response: The assessee may file acceptance of the variations proposed in the draft order or file objections, if any, to such variations.

- Final Assessment Order: In cases other than those referred to above, the National Faceless Assessment Centre conveys to the assessment unit to pass the final assessment order in accordance with the draft order. The assessment unit then passes the final assessment order and initiates penalty proceedings if necessary.

- Service of Final Order: The National Faceless Assessment Centre serves a copy of the final assessment order and notice for initiating penalty proceedings, if any, on the assessee, along with the demand notice specifying the sum payable or refund due.

This process ensures that the assessment order is passed in a transparent and systematic manner, with opportunities for the assessee to respond to any proposed variations. It also provides a structured mechanism for the assessment unit to finalize the assessment and initiate any necessary penalty proceedings.

Penalty Proceedings

The purpose of Penalty Proceedings is to address cases of concealment or inaccurate reporting of income during the faceless assessment process under Section 144B of the Income Tax Act. The penalty proceedings are intended to ensure compliance with tax regulations and deter taxpayers from providing incorrect or misleading information.

- Initiation of Penalty Proceedings: If during the course of faceless assessment under Section 144B, it is found that there is a case for initiation of penalty proceedings, the National Faceless Assessment Centre shall initiate such proceedings and follow the prescribed procedure.

- Referral to Assessing Officer: Upon initiating penalty proceedings, the National Faceless Assessment Centre refers the case to the Assessing Officer with jurisdiction for conducting the penalty proceedings as per Chapter XXI

- Integration with Penalty Provisions: The penalty proceedings are integrated with the penalty provisions of Chapter XXI of the Income Tax Act, ensuring that penalties are imposed in accordance with the applicable provisions

Penalty Proceedings under Section 144B involve the initiation of penalty proceedings for cases involving concealment or inaccurate particulars of income. Once the penalty proceedings are completed, the electronic records are transferred to the Assessing Officer for further actions.

Transfer of Electronic Records

The process of transferring electronic records under Section 144B of the Income Tax Act is a vital step in ensuring the seamless transition of information and documents.

- Completion of Assessment: After the completion of the assessment, the National Faceless Assessment Centre is responsible for transferring all electronic records of the case.

- Transfer to Assessing Officer: The electronic records are transferred to the Assessing Officer having jurisdiction over the said case for any action required under the provisions of the Act.

This process ensures that all relevant electronic records are securely transferred to the appropriate Assessing Officer, maintaining the integrity and confidentiality of the information.

Conclusion

In this part, we discussed the provisions related to Assessment and Penalties. In Part 4, we will go over Special Provisions for Complex Cases, Jurisdiction and Transfer of Cases.

Author: Parthvi Patel, United World School of Law

Advocate Aaditya Bhatt

Senior Standing Counsel Income Tax Department, Advocate Gujarat High Court. Aaditya combines his technical and legal expertise to deliver strategic counsel in litigation, constitutional, and regulatory matters. He represents clients before High Courts and Tribunals with a technology-driven approach.