Whatsapp

Whatsapp

Faceless Assessment Procedure under Section 144B of Income Tax Act – Part 2

Introduction

The Indian tax administration system has undergone a transformative evolution with the introduction of faceless assessment procedures. This revolutionary mechanism represents a fundamental shift from the traditional assessment system where physical interaction between taxpayers and tax authorities was the norm. The faceless assessment regime under Section 144B was conceived to address longstanding concerns about transparency, accountability, and efficiency in tax administration while simultaneously curbing opportunities for corruption and harassment of taxpayers. This initiative forms a crucial component of the government’s broader vision of “Transparent Taxation – Honouring the Honest” launched by the Prime Minister in August 2020.

The transition to faceless assessment represents more than just a technological upgrade. It embodies a comprehensive reimagining of how tax assessments should be conducted in the digital age. The system eliminates direct interaction between assessing officers and taxpayers, replacing it with a faceless, automated, and technology-driven process managed through centralized platforms. This transformation aims to create a level playing field for all taxpayers while ensuring that the assessment process remains fair, transparent, and efficient.

Legislative Framework and Statutory Provisions

The legal foundation for faceless assessment was established through the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020, which inserted Section 144B into the Income Tax Act, 1961 [1]. This provision came into effect from April 1, 2021, and provided the statutory basis for conducting assessments without physical interface between taxpayers and assessing authorities. The provision begins with a non-obstante clause, giving it overriding effect over other assessment provisions contained in the Act.

Section 144B mandates that assessments under Section 143(3) and Section 144 shall be made in a faceless manner through a prescribed procedure [2]. The section establishes that notwithstanding anything to the contrary contained in any other provisions of the Act, the assessment shall be conducted electronically without requiring the taxpayer to appear either personally or through an authorized representative before the income tax authority. This fundamental change eliminates the jurisdictional concept of assessment, replacing it with a dynamic, team-based approach operating through automated allocation systems.

The legislative framework creates several specialized units to handle different aspects of the assessment process. The National Faceless Assessment Centre serves as the central hub and sole point of contact between taxpayers and the department. Regional Faceless Assessment Centres operate under the supervision of Regional Principal Chief Commissioners to carry out assessments across different geographical regions. Assessment Units examine issues, gather materials to determine tax liabilities, and prepare draft assessment orders. Verification Units conduct inquiries, cross-verify records, examine books of accounts, and record statements when necessary. Technical Units provide expert opinions on specialized matters including law, accounting, information technology, forensics, valuation, and transfer pricing. Review Units examine draft assessment orders to ensure all facts, evidence, legal provisions, and relevant judicial precedents have been properly considered before finalization.

Prior to the insertion of Section 144B, the government had introduced the E-Assessment Scheme in 2019 through notification dated September 12, 2019. This scheme was later renamed as the Faceless Assessment Scheme and substantially amended through notification dated August 13, 2020 [3]. The scheme initially covered only scrutiny assessments under Section 143(3), but its scope was expanded to include best judgment assessments under Section 144 from assessment year 2020-21 onwards.

Constitutional Principles and Natural Justice

The faceless assessment mechanism under Section 144B operates within the framework of constitutional principles and natural justice that form the bedrock of Indian jurisprudence. The Supreme Court in the landmark judgment of Maneka Gandhi v. Union of India established that administrative actions affecting individual rights must adhere to principles of natural justice and that any procedure depriving a person of liberty must be just, fair, and reasonable [4]. This principle extends to quasi-judicial functions performed by tax authorities in making assessments.

Section 144B incorporates several procedural safeguards to ensure compliance with natural justice principles. The provision mandates that where a variation is proposed in the draft assessment order that is prejudicial to the assessee, a show cause notice must be issued providing the assessee an opportunity to explain why the assessment should not be completed as per the draft order. The assessee retains the right to request a personal hearing through video conferencing or telephony to present oral submissions, although this is subject to technological feasibility and approval by competent authorities [5].

The requirement of providing reasonable opportunity before passing orders prejudicial to taxpayers has been consistently upheld by courts. In several cases, courts have struck down assessment orders where adequate opportunity was not provided to respond to show cause notices or where requests for personal hearing were arbitrarily rejected without proper reasons. The Delhi High Court has clarified that while the scheme aims to minimize physical interface, it does not intend to eliminate the taxpayer’s right to be heard effectively [6].

Procedural Architecture of Faceless Assessment

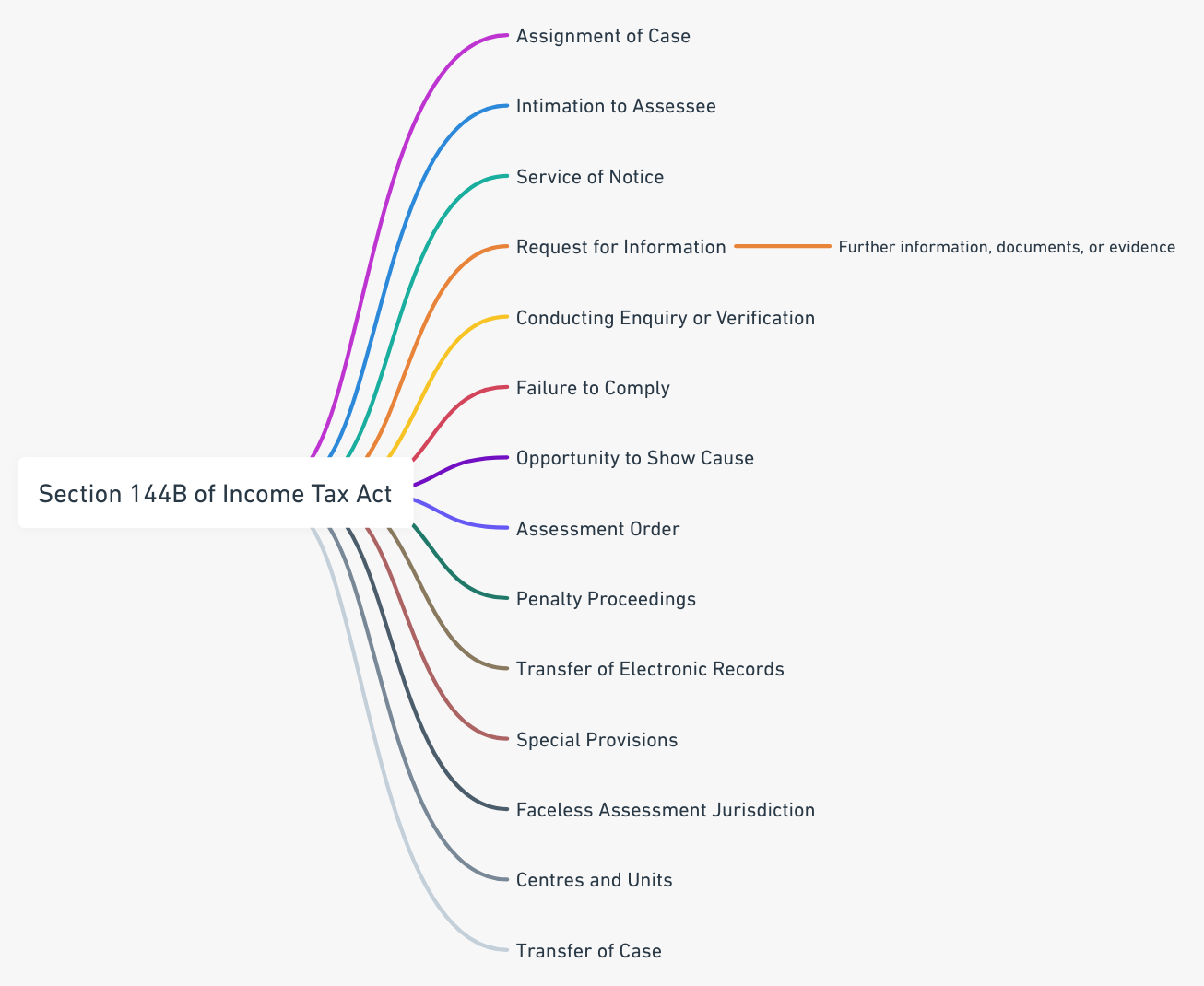

The faceless assessment process follows a structured workflow designed to ensure systematic examination while maintaining transparency. The procedure begins when the National Faceless Assessment Centre issues a notice under Section 143(2) to the assessee through the e-filing portal. The assessee is provided fifteen days from receipt of notice to file their response electronically through the designated portal. All communications between the National Faceless Assessment Centre and the assessee occur exclusively through electronic mode, utilizing the registered account on the income tax portal.

Once the response is received, the National Faceless Assessment Centre assigns the case to a specific Assessment Unit in any Regional Faceless Assessment Centre through an automated allocation system. This automated allocation ensures random distribution of cases, eliminating the possibility of manipulation or influence in case assignment. The Assessment Unit examines the return, response, and supporting documents to identify issues requiring detailed examination. Where additional information or documents are needed, the Assessment Unit communicates its requirements through the National Faceless Assessment Centre, which forwards the request to the assessee electronically.

If the Assessment Unit proposes variations that differ from the return filed by the assessee, a draft assessment order is prepared detailing the proposed additions or disallowances along with reasons and supporting evidence. This draft order is forwarded to a Review Unit in any Regional Faceless Assessment Centre for examination. The Review Unit verifies whether all relevant facts have been examined, legal provisions correctly applied, and judicial precedents considered. This two-tier review mechanism provides additional quality control to ensure accuracy and fairness in assessments.

After review, if variations are proposed, a show cause notice is issued to the assessee through the National Faceless Assessment Centre, providing an opportunity to contest the proposed variations. The assessee can submit written objections and may request a personal hearing through video conferencing. After considering the response and conducting hearing if requested, the Assessment Unit prepares the final assessment order which is served on the assessee electronically along with the demand notice specifying tax payable or refund due.

Judicial Interpretation and Case Law Developments

The implementation of faceless assessment has generated significant litigation, with several High Courts examining various aspects of the scheme’s constitutional validity and procedural compliance. Courts have consistently emphasized that the faceless nature of proceedings does not dilute procedural safeguards or natural justice requirements. In cases where assessment orders were passed before the expiry of time allowed for responding to show cause notices, courts have held such orders invalid and remanded matters back for fresh consideration after providing adequate opportunity [7].

The Delhi High Court has ruled that the word “may” used in the context of personal hearings should be construed as mandatory when dealing with quasi-judicial functions having civil consequences. The court held that faceless assessment does not mean no personal hearing, and where an assessee requests a hearing, it must be granted unless compelling reasons exist to deny it [8]. This interpretation balances the efficiency objectives of faceless assessment with fundamental requirements of natural justice.

Several courts have addressed situations where draft assessment orders were not issued despite being mandatory under the scheme. In such cases, courts have held that bypassing mandatory procedures constitutes a violation of statutory provisions that cannot be treated as mere procedural irregularity. The Bombay High Court in multiple cases has quashed assessment orders where the prescribed procedure under Section 144B was not followed, reaffirming that compliance with statutory procedure is jurisdictional and non-negotiable [9].

The question of jurisdiction in reassessment proceedings has also been subject to judicial scrutiny. Various High Courts have held that notices issued under Section 148 by Jurisdictional Assessing Officers instead of through the faceless mechanism violate the scheme’s mandatory provisions. Courts have emphasized that the faceless regime applies from the stage of issuing notices, and failure to comply with this requirement renders the entire proceeding invalid. However, there has been some divergence in judicial opinion on this issue, with different High Courts taking varying positions on whether non-compliance with faceless procedures necessarily invalidates the assessment.

Advantages and Implementation Challenges

The faceless assessment regime under Section 144B offers several significant advantages over the traditional system. It eliminates physical interface between taxpayers and assessing officers, thereby reducing opportunities for corruption, harassment, and subjective bias. The automated allocation system ensures random distribution of cases, preventing manipulation or influence in case assignment. The involvement of multiple units in the assessment process through a team-based approach enhances quality and consistency in decision-making. The centralized communication through a single portal simplifies compliance for taxpayers and creates a comprehensive electronic audit trail of all proceedings.

The scheme promotes transparency by ensuring all communications are documented electronically and accessible to taxpayers through their registered accounts. It enables optimal resource utilization through specialized units handling specific aspects of assessments based on their expertise. The system facilitates uniform application of law across different regions by standardizing procedures and enabling sharing of best practices. The digital infrastructure supporting faceless assessment enables data analytics and artificial intelligence tools to identify patterns and improve risk assessment capabilities.

Despite these advantages, implementation has encountered certain challenges. Technical glitches in the e-filing portal and communication systems have occasionally disrupted proceedings. The lack of face-to-face interaction can make it difficult to resolve complex factual or interpretational issues that benefit from detailed discussions. The quality of written submissions becomes critical in faceless proceedings, potentially disadvantaging taxpayers without sophisticated representation. Time constraints for responding to notices sometimes prove insufficient for gathering and presenting detailed evidence. The discretionary nature of granting personal hearings has led to inconsistency in application across different cases. Coordination among multiple units handling different aspects of the same assessment can sometimes cause delays or communication gaps.

Regulatory Framework and Notifications

The Central Board of Direct Taxes has issued several notifications and circulars to operationalize Section 144B and address implementation issues. The Faceless Assessment Scheme, 2020 notified on August 13, 2020 established the detailed procedural framework for conducting faceless assessments. This notification delineated the powers and functions of various units, prescribed timelines for different stages of assessment, and specified circumstances under which cases may be excluded from faceless assessment [10].

Subsequent notifications have expanded the scope of faceless proceedings to cover various other provisions including rectification of mistakes, giving effect to appellate orders, and penalty proceedings. The government has also excluded certain categories of cases from faceless assessment, including cases involving serious fraud, substantial tax evasion, international taxation matters, search and seizure cases, and cases with significant sensitivity. These exclusions recognize that certain complex or sensitive matters may benefit from traditional assessment approaches involving direct interaction.

The Central Board of Direct Taxes has issued clarificatory circulars addressing practical issues arising during implementation. These include clarifications on authentication of electronic records, conduct of personal hearings through video conferencing, handling of technical difficulties during proceedings, and procedures for seeking extension of time limits. The board has emphasized the importance of providing reasonable opportunities and maintaining principles of natural justice while implementing faceless assessment procedures.

Conclusion

The introduction of faceless assessment under Section 144B represents a transformative step in modernizing India’s tax administration. By leveraging technology to eliminate physical interface while maintaining procedural safeguards, the system aims to achieve greater efficiency, transparency, and accountability. The legislative framework provides comprehensive procedures for conducting assessments through centralized platforms utilizing automated allocation and team-based examination. Judicial interpretation has reinforced that the faceless nature does not diminish requirements of natural justice, particularly the right to be heard effectively before adverse orders are passed.

As the faceless assessment regime continues to evolve, ongoing refinements address implementation challenges while maintaining the core principles of fairness and transparency. The system demonstrates how technology can be effectively harnessed to transform traditional processes without compromising fundamental rights and procedural safeguards. For taxpayers, understanding the procedures, timelines, and rights under the faceless assessment framework is essential for effective compliance and protecting their interests during assessment proceedings. In Part 3, we shall discuss the provisions related to Assessment and Penalties.

REFERENCES

[1] The Income Tax Act, 1961, Section 144B. https://www.indiacode.nic.in/handle/123456789/1970

[2] ClearTax. (2025). Faceless Assessment Scheme Under Section 144B of Income Tax Act. https://cleartax.in/s/e-assessment-scheme-2019

[3] PwC India. (2020). Faceless Interface: A Paradigm Shift in Administration of the Income-tax Law. https://www.pwc.in/assets/pdfs/research-insights/faceless-interface-2020/faceless-interface.pdf

[4] Maneka Gandhi v. Union of India, AIR 1978 SC 597. https://indiankanoon.org/doc/1766147/

[5] IndiaFilings. (2025). Section 144B of Income Tax Act: Faceless Assessment. https://www.indiafilings.com/learn/section-144b-of-income-tax-act/

[6] TaxGuru. (2021). Latest Cases On – Principles Of Natural Justice – Faceless Assessment. https://taxguru.in/income-tax/latest-cases-principles-natural-justice-faceless-assessment.html

[7] Voice of CA. Recent Rulings on Faceless Assessment Scheme. https://www.voiceofca.in/siteadmin/document/RecentRulingsonFacelessAssessmentScheme.pdf

[8] SCC Times. (2022). Faceless Assessment Scheme Does Not Mean No Personal Hearing. https://www.scconline.com/blog/post/2022/01/17/faceless-assessment-scheme-does-not-mean-no-personal-hearing/

[9] TaxGuru. (2024). Faceless Assessment & Section 148: Jurisdictional Challenges & Recent Judgments. https://taxguru.in/income-tax/faceless-assessment-section-148-jurisdictional-challenges-recent-judgments.html

[10] Lexology. (2022). Faceless Assessment Scheme under the Income Tax Act, 1961. https://www.lexology.com/library/detail.aspx?g=229dd89f-da4f-4564-8bce-43712e5c58b1