Whatsapp

Whatsapp

Financial Debt and Joint Venture Investments: A Comprehensive Legal Analysis Under the Insolvency and Bankruptcy Code

Introduction

The Insolvency and Bankruptcy Code, 2016 (hereinafter referred to as “the Code”) represents a watershed moment in India’s commercial jurisprudence, fundamentally transforming how financial distress and corporate insolvency are addressed in the country. Since its enactment, the Code has been instrumental in establishing a clear framework for determining creditor rights, prioritizing claims, and facilitating the revival or liquidation of distressed corporate entities. However, the application of the Code to various financial arrangements has been subject to extensive judicial interpretation, particularly concerning the distinction between genuine financial debt and commercial investments that share profit and risk. One of the most contentious areas that has emerged in insolvency jurisprudence relates to joint venture arrangements and whether investments made under such collaborations qualify as financial debt under the statutory definitions provided in the Code. This question carries significant practical implications because the classification determines whether an investor can initiate insolvency proceedings as a financial creditor or whether their claim must be treated differently. The National Company Law Appellate Tribunal’s judgment in RealPro Realty Solutions Pvt Ltd vs Sanskar Projects and Housing Ltd [1] has provided crucial clarity on this issue, establishing important precedents for distinguishing between genuine creditor-debtor relationships and joint venture partnerships.

The significance of this distinction cannot be overstated. Financial creditors, as defined under the Code, enjoy privileged status in insolvency proceedings, including the right to trigger the Corporate Insolvency Resolution Process (CIRP) and participate in the Committee of Creditors with voting rights. Conversely, entities that are deemed to be business partners or investors rather than creditors do not enjoy these rights, regardless of the quantum of money invested or the terms of repayment stipulated in their agreements. The judicial interpretation of these arrangements therefore has far-reaching consequences for how businesses structure their collaborations and how courts evaluate the substance of financial transactions beyond their formal documentation.

The Legislative Framework: Understanding Financial Debt and Financial Creditors Under the IBC

Defining Financial Creditors

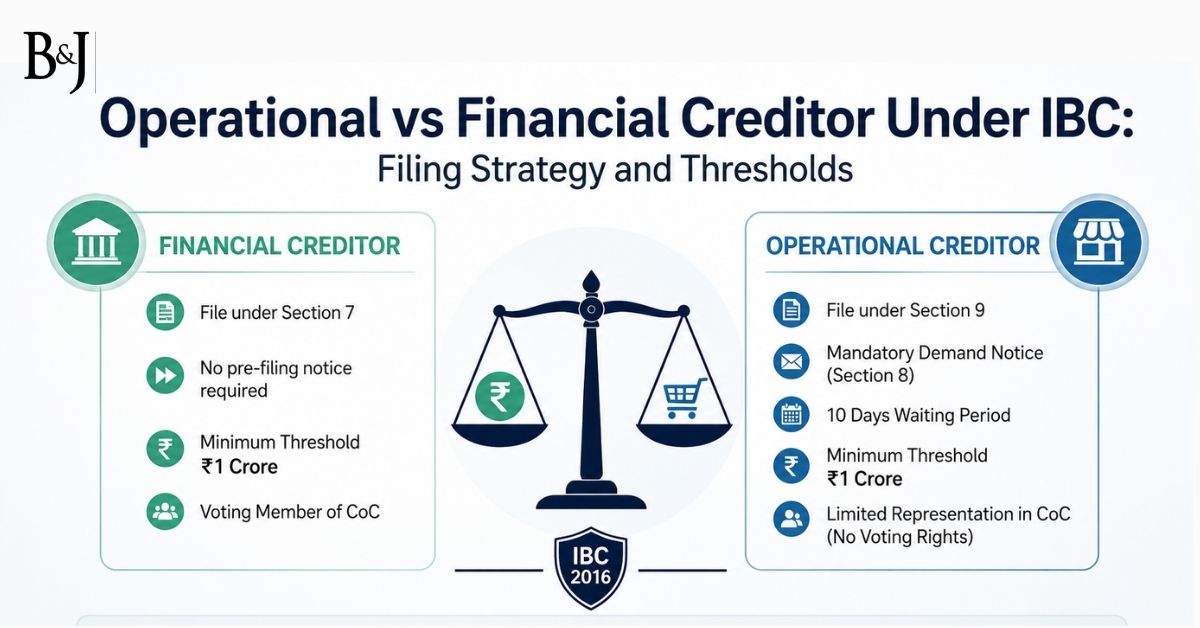

The architecture of the Insolvency and Bankruptcy Code rests fundamentally on the distinction between different classes of creditors and their respective rights in insolvency proceedings. Section 5(7) of the Code defines a “financial creditor” as any person to whom a financial debt is owed, including persons to whom such debt has been legally assigned or transferred [2]. This definition appears straightforward on its face, but its practical application requires a detailed understanding of what constitutes financial debt in the first place. The classification as a financial creditor is not merely a matter of nomenclature; it determines the substantive rights available to a claimant in insolvency proceedings, including the critical ability to initiate CIRP and participate in decision-making through the Committee of Creditors.

The legislative intent behind creating this distinct category of financial creditors stems from the recognition that entities that provide debt capital to businesses have different economic interests and risk profiles compared to those who supply goods and services. Financial creditors typically assess the viability of the corporate debtor’s business before extending credit, monitor the financial health of the debtor during the term of the loan, and have a continuing stake in the debtor’s solvency. This ongoing relationship and assessment capability justifies their privileged position in the resolution process, where they collectively determine the fate of the corporate debtor through the Committee of Creditors.

The Concept of Financial Debt

Section 5(8) of the Code provides an elaborate definition of “financial debt” that forms the cornerstone for determining who qualifies as a financial creditor. The provision states that financial debt means a debt along with interest, if any, which is disbursed against the consideration for the time value of money. This central concept of “consideration for the time value of money” serves as the defining characteristic that separates financial debt from other forms of commercial obligations. The provision further includes within its ambit various specific categories including money borrowed against payment of interest, amounts raised through debt securities, amounts due under deferred payment arrangements, amounts due under finance leases, and amounts raised under securitization or factoring transactions [3].

The legislative emphasis on “time value of money” as the determinative factor reflects a sophisticated understanding of financial economics. The time value of money recognizes that money available at present is worth more than the same amount in the future due to its potential earning capacity. When a lender provides funds to a borrower, the compensation for parting with liquidity and bearing the risk of non-repayment is typically structured as interest or a fixed return that reflects this time value. This distinguishes genuine lending from equity investment or profit-sharing arrangements where returns are contingent on business performance rather than being compensation for the passage of time.

The inclusive nature of the definition in Section 5(8) ensures that various modern financial instruments and arrangements can be brought within the fold of financial debt, provided they meet the core requirement of being consideration for the time value of money. This approach prevents sophisticated parties from structuring transactions in ways that avoid the application of the Code while maintaining the economic substance of a lending arrangement. However, it also means that courts must look beyond the form of transactions to examine their true economic character, particularly in cases involving hybrid instruments that combine features of both debt and equity.

Joint Ventures in the Indian Legal Context: Characteristics and Legal Treatment

Understanding Joint Venture Structures

Joint ventures represent a distinct category of commercial collaboration where two or more parties combine resources, expertise, and capital to pursue a specific business objective while sharing both the risks and rewards of the enterprise. Unlike traditional creditor-debtor relationships, joint ventures are characterized by mutual participation in management, shared decision-making authority, and proportional distribution of profits and losses based on agreed formulas. The essence of a joint venture lies in the partnership nature of the arrangement, where parties act as co-venturers rather than as lender and borrower.

In the Indian context, joint ventures have become particularly prevalent in sectors such as real estate development, infrastructure projects, manufacturing, and technology ventures. These collaborations often involve one party bringing financial resources while another contributes land, expertise, regulatory approvals, or market access. The arrangements are typically documented through detailed joint venture agreements that specify capital contributions, profit-sharing ratios, management structures, exit mechanisms, and dispute resolution procedures. However, the terminology used in these agreements does not necessarily determine their legal character for purposes of insolvency law.

The legal treatment of joint ventures under various Indian statutes has evolved through judicial interpretation. Under the Indian Contract Act, 1872, joint ventures are generally treated as a form of partnership, though they may be limited to a specific project or duration. The Income Tax Act recognizes joint ventures as distinct entities for tax purposes in certain circumstances. However, the critical question for insolvency law is whether investments made under joint venture arrangements constitute financial debt that would entitle the investor to the status and rights of a financial creditor under the Code.

Distinguishing Investment from Lending

The fundamental distinction that courts must draw in these cases is between money advanced as a loan (which creates a creditor-debtor relationship) and money invested as capital contribution in a joint enterprise (which creates a partnership or co-ownership relationship). This distinction turns on several factors beyond the mere labeling of payments or the inclusion of repayment clauses in agreements. Courts examine the entire structure of the arrangement, including whether returns are fixed or contingent on profits, whether the contributor has any management rights or obligations, whether risks and rewards are shared proportionally, and whether the agreement contemplates joint ownership of assets or outcomes.

The difficulty in making this distinction arises because modern joint venture agreements often incorporate features that superficially resemble debt arrangements. They may include provisions for return of capital, timelines for such returns, and even specify certain fixed components of return. However, when these provisions are examined in the context of the overall arrangement, particularly clauses relating to profit sharing, risk allocation, and management participation, the true nature of the relationship becomes clearer. The courts have consistently held that the substance of the transaction rather than its form must guide the legal characterization.

The RealPro Realty Solutions Judgment: Facts and Legal Analysis

Factual Matrix of the Case

The case of RealPro Realty Solutions Pvt Ltd vs Sanskar Projects and Housing Ltd presented the National Company Law Appellate Tribunal with a quintessential example of the conflict between joint venture arrangements and claims of financial creditor status under the Code. The appellant, RealPro Realty Solutions Pvt Ltd, had entered into an agreement with the respondent, Sanskar Projects and Housing Ltd, for the development of real estate property. Under the terms of this agreement, RealPro invested substantial funds in the project, with the understanding that it would receive returns based on the project’s profitability and the successful sale of developed units.

When disputes arose between the parties and the project encountered financial difficulties, RealPro sought to invoke its rights as a financial creditor under Section 7 of the Code, claiming that its investment constituted financial debt. The appellant argued that since the agreement specified repayment of the invested amount along with returns, it should be treated as a lending arrangement rather than a joint venture investment. This position, if accepted, would have entitled RealPro to initiate CIRP against Sanskar Projects and participate in the resolution process as a financial creditor with voting rights in the Committee of Creditors.

The respondent contested this characterization, arguing that the agreement clearly established a joint venture relationship where both parties were co-developers sharing the risks and rewards of the real estate project. According to Sanskar Projects, the returns contemplated under the agreement were explicitly linked to the success of the development and sale of property, making them profit-sharing arrangements rather than interest or fixed returns that would characterize a debt relationship. The company emphasized that RealPro had participated in project decisions and had agreed to share both profits and potential losses, which are hallmarks of a partnership rather than a creditor-debtor relationship.

The NCLAT’s Reasoning and Conclusions

The National Company Law Appellate Tribunal, in a carefully reasoned judgment delivered by a coram consisting of Justice Ashok Bhushan (Chairperson), Mr. Barun Mitra (Technical Member), and Mr. Arun Baroka (Technical Member), undertook a thorough analysis of the agreement between the parties and the applicable legal principles. The Tribunal began by articulating a clear definition of joint ventures, stating that a joint venture represents a combination of two or more parties or entities that seeks the development of any enterprise or project for profit and necessarily entails sharing the risks associated with its development [1].

Examining the specific terms of the agreement between RealPro and Sanskar Projects, the NCLAT observed that the arrangement clearly manifested shared liability for profit. The Tribunal noted that when such shared liability for profit is explicitly incorporated into the contractual framework, it becomes evident that both parties are development partners and co-sharers in the development of the subject property. This observation was crucial because it shifted the focus from isolated clauses about repayment to the overall economic substance of the relationship. The Tribunal emphasized that the terms of the agreement laid the foundations of a legal and binding relationship with mutual financial obligations towards each other, rather than a unilateral obligation of the debtor to repay a creditor.

The most significant conclusion reached by the NCLAT was that the appellant, by virtue of the funds invested under the terms of the agreement, could not claim the status and benefits of a financial creditor as defined under Section 5(7) of the Code. This conclusion flowed from the Tribunal’s analysis that the transaction was in the nature of an investment for profit rather than a disbursement for the time value of money. Since the essential characteristic of financial debt under Section 5(8) is that it must be disbursed against consideration for the time value of money, and since the present arrangement was structured around profit-sharing rather than compensation for time value, it did not fall within the definition of financial debt.

The judgment clarified that the mere fact that an agreement specifies certain timelines for returns or uses terminology that might suggest a debt relationship is insufficient to convert a joint venture investment into financial debt. The Tribunal adopted a substance-over-form approach, looking at the economic reality of the transaction rather than being swayed by drafting choices made by the parties. This approach aligns with the broader jurisprudential principle that courts must examine the true nature of transactions, particularly in insolvency proceedings where the classification determines significant rights and priorities among competing stakeholders.

Implications for Real Estate Joint Ventures and Development Agreements

The Real Estate Sector Context

The real estate development sector in India has historically relied heavily on various forms of collaborative financing and joint development arrangements. Given the capital-intensive nature of real estate projects, the long gestation periods involved, and the regulatory complexities of land development, it is common for developers to enter into arrangements with financial partners who provide capital in exchange for a share of the project’s profits. These arrangements have become even more prevalent in the wake of the Real Estate (Regulation and Development) Act, 2016, which imposed stricter controls on project financing and use of customer advances.

Prior to the RealPro judgment and similar precedents, there was considerable uncertainty about whether these development partners could claim financial creditor status if disputes arose. Some parties attempted to structure their arrangements with explicit repayment clauses and interest-like returns, hoping to secure the advantageous position of financial creditors while maintaining the flexibility and profit potential of joint venture arrangements. The RealPro judgment has effectively foreclosed this strategy by clarifying that courts will examine the overall structure of the arrangement rather than isolated provisions.

Practical Consequences for Structuring Collaborations

The judgment has several important practical implications for how parties structure their real estate collaborations and other joint venture arrangements. First, it establishes that parties cannot simply label an arrangement as a loan or include repayment clauses to secure financial creditor status if the underlying economic relationship is one of shared risk and profit. This means that developers and investors must be more deliberate in choosing between genuine financial debt and joint venture structures, understanding that each comes with different rights and remedies in the event of disputes or insolvency.

Second, the judgment provides greater protection to corporate debtors against strategic use of insolvency proceedings by dissatisfied joint venture partners. If every joint venture partner who invested capital could threaten or initiate CIRP proceedings by claiming financial creditor status, it would expose companies to inappropriate use of the insolvency process for commercial disputes. By clarifying that joint venture investments do not constitute financial debt, the judgment ensures that the CIRP mechanism is reserved for genuine cases of financial distress and creditor default rather than becoming a pressure tactic in business disputes.

Third, the decision encourages transparency and proper characterization of relationships from the outset. Parties entering into collaborations must clearly determine whether they are creating a creditor-debtor relationship or a joint venture partnership and structure their agreements accordingly. This clarity benefits all stakeholders by reducing disputes over the nature of the relationship and the rights available to each party. It also ensures that financial statements and disclosures accurately reflect the company’s obligations, including distinctions between financial debt and joint venture investments, aligning reporting with the true economic substance of the arrangements.

The Broader Jurisprudence on Financial Debt Under the IBC

The “Time Value of Money” Test

The RealPro judgment must be understood in the context of the broader jurisprudence that has developed around the interpretation of financial debt under the Code. Indian courts, including the Supreme Court, have consistently emphasized that the defining characteristic of financial debt is that it must be disbursed against consideration for the time value of money. This principle has been applied across various types of transactions to distinguish genuine debt from other commercial arrangements [4].

The time value of money concept recognizes that when a lender provides funds to a borrower, the compensation is primarily for the loss of liquidity and the passage of time, rather than for the commercial success or failure of a particular venture. Interest on a loan, for example, accrues based on time and the principal amount, regardless of whether the borrower’s business is profitable. In contrast, returns under a profit-sharing arrangement are inherently contingent on business performance and are not guaranteed merely by the passage of time. This fundamental distinction guides courts in classifying ambiguous arrangements.

Related Precedents and Judicial Trends

The principles established in the RealPro judgment are consistent with other decisions where courts have examined the nature of investments and contributions in collaborative business ventures. The judiciary has shown a consistent approach of examining the totality of circumstances and the economic substance of arrangements rather than being influenced by the terminology used by parties or isolated contractual provisions. This approach reflects a mature understanding that sophisticated parties may attempt to structure transactions in ways that secure favorable legal treatment while maintaining the economic characteristics of a different type of arrangement.

Courts have also been attentive to the purpose and policy underlying the Code’s distinction between financial creditors and other stakeholders. The legislative design gives financial creditors significant rights and control in the insolvency resolution process because they are understood to be external capital providers who assess and monitor the debtor’s creditworthiness. In contrast, joint venture partners or equity investors are treated as having voluntarily assumed business risks in exchange for potentially higher returns, and therefore should not have the same priority or control as genuine lenders in insolvency proceedings.

Distinguishing Financial Debt from Operational Debt and Other Commercial Obligations

The Operational Creditor Category

While the RealPro judgment focused on distinguishing joint venture investments from financial debt, it is important to understand how both of these categories differ from operational debt. Section 5(20) of the Code defines operational debt as a claim in respect of provision of goods or services, including employment, or a debt in respect of repayment of dues arising under any law for the time being in force and payable to the Central Government, State Government, or any local authority [5]. Operational creditors, while having the right to initiate CIRP under Section 9 of the Code, do not participate in the Committee of Creditors unless their claims exceed certain thresholds, and even then their participation is limited.

The distinction between financial and operational debt reflects different policy considerations. Operational creditors supply goods and services in the ordinary course of business, and while their claims are important, they typically do not have the same ongoing financial stake or monitoring capacity as financial creditors. The Code’s structure recognizes these differences by giving operational creditors the ability to trigger insolvency proceedings (to prevent debtors from ignoring their obligations to suppliers and service providers) while reserving control over the resolution process primarily to financial creditors who are better positioned to assess the viability of revival plans.

Hybrid Instruments and Complex Financial Arrangements

Modern corporate finance increasingly involves sophisticated instruments that combine features of debt and equity, such as convertible debentures, preference shares with fixed returns, and various forms of mezzanine financing. The classification of these instruments under the Code has been the subject of considerable litigation and legal analysis. Courts have approached these cases by examining the predominant characteristics of the instrument and the true economic relationship it creates between the parties.

The key inquiry in cases involving hybrid instruments is whether the compensation provided to the investor is primarily for the time value of money or for assuming business risk. If a convertible debenture pays regular interest and the conversion option is merely an additional feature, it is more likely to be treated as financial debt. However, if the returns are primarily contingent on equity conversion and business performance, with minimal fixed return component, it may be treated more like an equity investment. The RealPro judgment’s emphasis on examining the overall structure and economic substance of arrangements provides guidance for analyzing these complex instruments.

Regulatory and Commercial Implications

Impact on Project Financing and Structuring

The clarification provided by the RealPro judgment has significant implications for how companies structure their project financing arrangements, particularly in capital-intensive sectors like real estate, infrastructure, and manufacturing. Companies and their advisors must now be more careful in distinguishing between genuine debt financing (which may be more expensive but provides clearer creditor protections) and joint venture arrangements (which may be more flexible but do not provide financial creditor rights). This increased clarity should lead to better-structured transactions that accurately reflect the parties’ intentions and rights.

From a regulatory perspective, the judgment reinforces the importance of accurate financial reporting and disclosure. Companies must ensure that their financial statements properly classify different types of funding sources, distinguishing between financial debt, operational liabilities, and capital contributions or joint venture arrangements. This accuracy is important not only for compliance with accounting standards but also because it affects how stakeholders, including potential creditors and investors, assess the company’s financial health and risk profile [6].

Considerations for Insolvency Professionals and Resolution Applicants

For insolvency professionals who must verify and admit claims in CIRP proceedings, the RealPro judgment provides important guidance on evaluating claims from parties who may have provided funds under various arrangements. Insolvency professionals must look beyond the terminology used in agreements and examine the substantive nature of the relationship to determine whether a claimant qualifies as a financial creditor. This requires careful analysis of joint venture agreements, shareholders’ agreements, and other collaboration documents to assess whether the funds were advanced as loans or as investments in a joint enterprise.

Resolution applicants and potential investors in distressed companies also benefit from this clarity. When conducting due diligence on a company undergoing CIRP, they can better assess the nature and priority of various claims. Understanding which parties are true financial creditors and which are joint venture partners or equity investors helps in valuing the company, negotiating with stakeholders, and structuring resolution plans. It also helps in identifying potential challenges to the classification of claims that might affect the resolution process or the enforceability of a resolution plan.

International Perspectives and Comparative Analysis

Treatment of Joint Ventures in Other Jurisdictions

The issue of how joint venture investments are treated in insolvency proceedings is not unique to India. Jurisdictions around the world have grappled with similar questions about distinguishing debt from equity and determining the rights of various types of investors in insolvency contexts. In the United Kingdom, for example, courts have developed extensive jurisprudence around the characterization of instruments and arrangements, emphasizing substance over form and examining the true nature of the commercial relationship between parties [7].

The United States bankruptcy system similarly distinguishes between creditors and equity holders, with important implications for voting rights, priority of claims, and distribution of assets. American courts have examined numerous cases involving hybrid securities and complex financing arrangements, developing principles that look at factors such as subordination provisions, management rights, profit participation, and risk allocation to determine the true character of an investment. While the specific legal frameworks differ, there is a common thread across jurisdictions of examining economic substance rather than being bound by contractual labels.

Lessons from International Best Practices

International experience suggests several best practices that are relevant to the Indian context following the RealPro judgment. First, clear documentation that accurately reflects the intended nature of the relationship is crucial. Parties should avoid mixing debt and equity features in ways that create ambiguity about the nature of the arrangement. Second, consistent treatment across different legal and regulatory contexts (such as tax, accounting, and insolvency law) helps reduce disputes and uncertainty. Third, periodic review and assessment of arrangements can help identify potential classification issues before they become problematic in insolvency or dispute scenarios.

Conclusion

The National Company Law Appellate Tribunal’s judgment in RealPro Realty Solutions Pvt Ltd vs Sanskar Projects and Housing Ltd represents a significant contribution to the evolving jurisprudence under the Insolvency and Bankruptcy Code. By clearly establishing that joint venture investments structured around profit-sharing do not constitute financial debt merely because they include provisions for return of capital or specify timelines for such returns, the Tribunal has provided much-needed clarity for the real estate sector and other industries that rely on collaborative financing arrangements.

The judgment’s emphasis on examining the economic substance of transactions rather than their formal documentation reflects a sophisticated understanding of modern commercial relationships and prevents parties from gaming the system by superficially structuring joint ventures to resemble debt arrangements. This approach protects the integrity of the insolvency process by ensuring that CIRP proceedings are initiated only by genuine financial creditors rather than becoming a tool for commercial disputes between business partners.

For businesses, investors, and legal practitioners, the RealPro judgment underscores the importance of careful structuring and documentation of commercial relationships. Parties must be clear from the outset whether they are entering into a creditor-debtor relationship or a joint venture partnership, and must structure their agreements consistently with that intent. The judgment also highlights the need for proper classification and disclosure of different types of funding sources, including financial debt and joint venture investments, in financial statements and regulatory filings.

Looking forward, the principles established in this judgment will likely influence how courts approach other cases involving hybrid financial instruments and complex commercial arrangements. The focus on substance over form and the examination of whether compensation is for time value of money or for profit participation provides a workable framework for analyzing a wide range of transactions. As Indian insolvency law continues to mature through judicial interpretation, decisions like RealPro contribute to building a coherent and predictable legal framework that balances the rights of different stakeholders while facilitating the core objectives of the Code: maximizing value, promoting entrepreneurship, balancing interests, and ensuring timely resolution of insolvency.

The judgment serves as a reminder that the Code’s careful distinction between different classes of creditors and stakeholders serves important policy purposes. Financial creditors are given privileged status because they are external capital providers who assess creditworthiness and monitor financial health. Joint venture partners, in contrast, are willing participants in business ventures who share both risks and rewards. Maintaining this distinction ensures that the insolvency resolution process functions as intended, with decision-making power vested in those who are best positioned to assess and execute revival strategies. The RealPro judgment’s clear articulation of these principles provides valuable guidance on the treatment of financial debt and joint venture investments for all participants in India’s insolvency ecosystem and contributes to the ongoing development of a robust and effective insolvency regime.

References

[1] RealPro Realty Solutions Pvt Ltd vs Sanskar Projects and Housing Ltd, National Company Law Appellate Tribunal, New Delhi. Available at: https://ibclaw.in/realpro-realty-solutions-pvt-ltd-vs-sanskar-projects-and-housing-ltd-nclat-new-delhi/

[2] The Insolvency and Bankruptcy Code, 2016, Section 5(7) – Definition of Financial Creditor. Available at: https://www.indiacode.nic.in/show-data?actid=AC_CEN_2_11_00055_201631_1517807328273&orderno=7

[3] IBC Laws. “Section 7 of IBC – Initiation of Corporate Insolvency Resolution Process by Financial Creditor.” Available at: https://ibclaw.in/section-7-initiation-of-corporate-insolvency-resolution-process-by-financial-creditor-chapter-ii-corporate-insolvency-resolution-processcirp-part-ii-insolvency-resolution-and-liquidation-for-corpor/

[4] Hiremath, Chetan. “Section 5(8) of IBC – What qualifies as Financial Debt.” LinkedIn Article, December 7, 2023. Available at: https://www.linkedin.com/pulse/section-58-ibc-what-qualifies-financial-debt-chetan-hiremath-2evpc

[5] IBC Laws. “Distinction in Treatment of Financial Creditors vs. Operational Creditors under IBC.” Available at: https://ibclaw.in/distinction-in-treatment-of-financial-creditors-vs-operational-creditors-by-vidushi-puri/

[6] Insolvency and Bankruptcy Board of India. “Discussion Paper on Financial Creditors in Corporate Insolvency Resolution Process.” Available at: https://ibbi.gov.in/Agenda_8_210917.pdf

[7] Legal Service India. “Financial Creditor vs Operational Creditor under IBC.” Available at: https://www.legalserviceindia.com/legal/article-6391-financial-creditor-vs-operational-creditor-under-ibc.html

[8] Indian Kanoon. “RealPro Realty Solutions Pvt Ltd vs Sanskar Projects and Housing Ltd Judgment.” Available at: https://indiankanoon.org/doc/165460821/

[9] Ministry of Corporate Affairs. “The Insolvency and Bankruptcy Code, 2016 – Full Text.” Available at: https://www.mca.gov.in/Ministry/pdf/TheInsolvencyandBankruptcyofIndiaCode2016.pdf

Authorized by Prapti Bhatt